Financial Fragmentation: How Geopolitical Risks Are Altering Global Payment Flows

The radical uncertainty of this risk type should not be underestimated.

The radical uncertainty of this risk type should not be underestimated.

By Julia Chong

By Julia Chong

In this year’s Global Payments Report, management consulting firm McKinsey estimate that global payments flow in 2023 hit an all-record high of USD1.8 quadrillion with a revenue pool of USD2.4 trillion on the back of 3.4 trillion transactions. This represents a 35% share of total banking revenue and indicates the severe knock-on effects a change in global payment systems can have on the financial system.

The fact that these record numbers come at a time of heightened geopolitical upheaval is cause for concern. Notably, the Russia-Ukraine conflict and deteriorating US-China relations have negatively impacted cross-border investment portfolios and bank credit allocation.

In banking, although the risk function sits squarely under the chief risk officer’s purview, the treatment of geopolitical risk is often left out of the equation, or at best, treated as a subjective touchy-feely sort of analysis mostly because it is viewed as an ambiguity compared to other quantified risks under the Basel regime.

Unlike loan default rates or tiered capital allocation rules, financial institutions cannot rely on traditional, quantifiable risk indicators when measuring geopolitical risk. The closest guidance that the Basel Committee on Banking Supervision has issued is its consultative document on Guidelines for Counterparty Credit Risk Management released on 30 April 2024 which states:

“Banks should ensure, at the point of onboarding, that their processes consider and assess non-financial risks as part of the credit risk decision-making process. Banks should also establish an escalation process and clear communication channels for the review of non-financial risks. For instance, banks should appropriately characterise the intersection between CCR (counterparty credit risk) and geopolitical or country risk. This is a process that may benefit from consultation with the legal department at the point of onboarding…These non-quantifiable risks can transform into CCR over the longer term even in cases where no direct impact on the probability of default can be seen.”

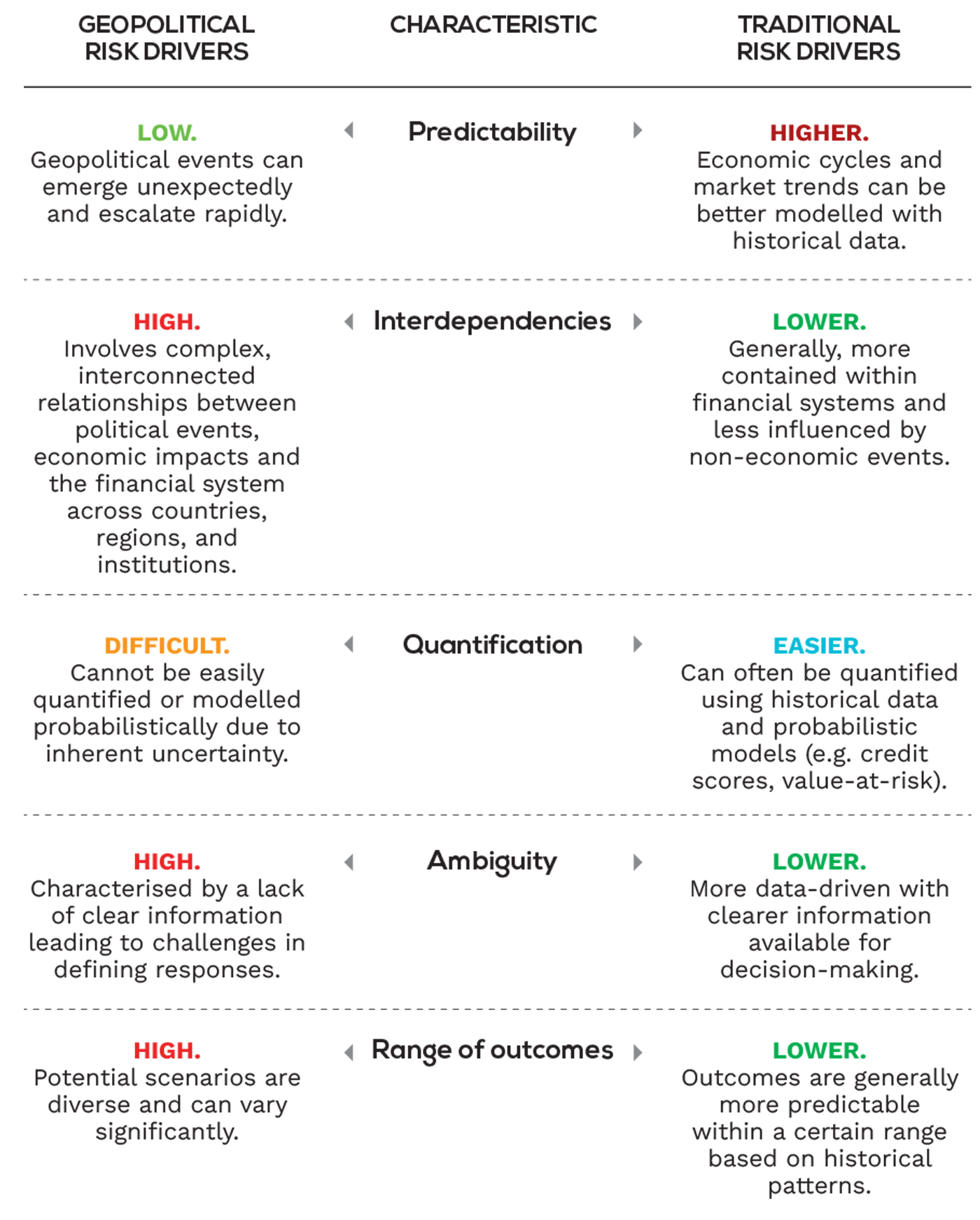

As vague as such advice may seem, geopolitical risk drivers are no less important than traditional risk drivers but because of the differences, as shown in Table 1, they should be assessed differently to the other types of risk that currently make up the arsenal of back-office risk calculations.

Although geopolitical instability seems a distant occurrence for banks in the Asia-Pacific region, it is imperative that they be on the lookout for future radical shifts in the payments and settlements landscape.

For instance, SWIFT (Society for Worldwide Interbank Financial Telecommunication) is the main messaging network through which international payments are initiated. Although very few banks in the region were directly affected by the sudden ban by SWIFT against Russian banks in 2022, the waves that reverberated throughout Asian financial markets were real.

An immediate circular by the Monetary Authority of Singapore (MAS) to local financial institutions (FIs) cautioned the sector about heightened risks and to take “appropriate measures to manage any legal, reputational, and operational risks arising from the sanctions” imposed on Russia with regard to the ongoing Ukraine conflict.

“FIs should also continue to stay vigilant to any suspicious transactions or flow of funds, and apply enhanced customer due diligence in higher-risk situations,” an MAS spokesperson told Asian Banking & Finance in response to its queries.

Under such volatile geopolitical circumstances, prudence is warranted.

The International Monetary Fund’s (IMF) Global Financial Stability Report issued in April 2023 highlights: “Financial fragmentation induced by geopolitical tensions could have potentially important implications for global financial stability by affecting the cross-border allocation of capital, international payment systems, and asset prices.”

The international funder estimates that a one-standard-deviation increase in geopolitical tensions between an investing and a recipient country, such as the US and China, could reduce cross-border portfolio and bank allocation by about 15%. Other financial stability risks for the global banking sector include a sudden reversal of cross-border credit and investments, increased debt-rollover risks, and higher funding costs for banks.

Across the board, all risk indicators confirm geopolitical tensions are increasing. The latest IMF working paper, Geopolitical Proximity and the Use of Global Currencies, published this September, reports that the Geopolitical Risk Index, an aggregate index that measures the number of adverse geopolitical events, has doubled in recent years. The global Trade Policy Uncertainty Index has also reached a historic high due to increased cross-border trade restrictions and foreign investment controls.

The authors, Jakree Koosakul, Longmei Zhang, and Maryam Zia, write: “Accordingly, persistent geopolitical tensions could significantly reshape cross-border capital flows and influence countries’ currency preferences vis-à-vis foreign exchange reserves, international payments, and trade invoicing.

“Since the end of World War II, the US dollar has been the dominant currency for international transactions, accounting for more than 60% of the total, followed by the euro and a few other currencies. However, increasing geopolitical tensions may impact decisions on currency usage and the payment network underlying it. This paper aims to shed light on the extent to which geopolitical factors affect currency usage, along with traditional economic factors, such as trade, financial linkages, and geographical distance.”

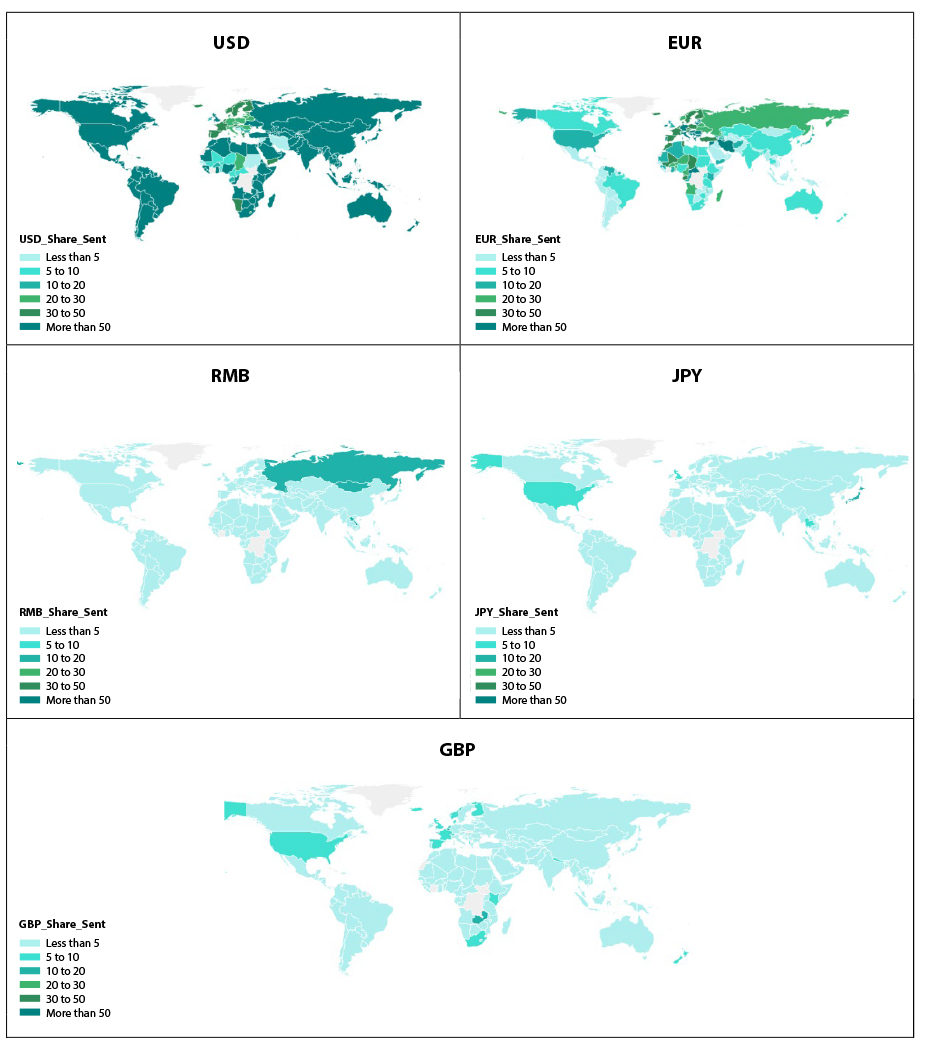

Examining the IMF’s basket of five special drawing rights (SDR) currencies – the US dollar, the euro, the Chinese renminbi, the Japanese yen, and the British pound sterling – and how their use varied with the level of geopolitical tensions, the researchers were able to determine the effect of geopolitical tensions on the use of global currencies in cross-border transactions.

Based on SWIFT data, global currency shares indicate significant regional variations. Figure 1 shows the extent of use of the five SDR currencies in cross-border payments across regions.

“While the US dollar has broad dominance, accounting for more than half of payments in most regions, the euro plays an eminent role in most of Europe and parts of Africa. The renminbi has gained traction in parts of Asia, such as Mongolia and Laos,” the report states.

“Interestingly, the US dollar has a larger presence in China for cross-border payments than the RMB itself. Outside of Japan, the Japanese yen is mainly present in Thailand’s cross-border transactions. The British pound is frequently used in Europe and parts of Africa.”

Cross-border payment networks used for international settlements have been traditionally US dominated. The most widely used, SWIFT, although headquartered in Belgium, is US controlled. The payment network has often been seen to be used as a tool to achieve US foreign policy objectives. An interview with two of its former executives in 2021 quotes them as saying that, “No bank can afford to lose access to the US payment system. If overseas banks do not comply with US sanctions, the US can simply forbid its banks to process dollar transactions for them.”

In recent times, several alternative payment systems and/or new technological platforms have come to the fore:

Amid increasing sanctions and escalating tensions, these growing alternatives for the financial sector signal a change in tides as countries and blocs move (albeit slowly) towards de-dollarisation.

Although the current global payment architecture is not even close to a shift in the status quo, the increasing prominence of alternative systems and platforms is something that banks should have on their radar at all times. The IMF recommends that “[P]olicymakers need to be aware of potential financial stability risks associated with a rise in geopolitical tensions and devote resources to their identification, quantification, management, and mitigation.”

Navigating the future calls for every bank to ensure its risk management framework robustly accounts for direct and indirect geopolitical risks.

A fine line to tread, for some more than others.

Julia Chong is a content analyst and writer at Akasaa, a boutique content development and consulting firm.