Never to be Bedfellows?

The divide between crypto and banking proper looms larger than ever.

The divide between crypto and banking proper looms larger than ever.

By Angela SP Yap and Kannan Agarwal

By Angela SP Yap and Kannan Agarwal

On 27 January 2023, the Federal Reserve Board (FRB) rejected the application of Custodia Bank, a special purpose depository institution (SPDI), for the opening of a master account with the Federal Reserve System.

Founded by its CEO and ex-Morgan Chase banker Caitlin Long, Custodia is an uninsured state-chartered bank that provides a regulated path for crypto companies to access banking services. A master account with the Federal Reserve would have given the bank direct access to the national payment and settlement system, cutting out the high costs it currently incurs through intermediary financial institutions because of its SPDI status.

The FRB denied its application based on two grounds: that Custodia’s risk management frameworks were not sufficient to address crypto risks; and that it also was involved in “novel and untested crypto activities that include issuing a crypto asset on open, public and/or decentralised networks.”

In response, Custodia sued the FRB, contending that the denial was improper and the latter was statutorily compelled to grant it a master account in accordance with US Code Service 248a whereby “all Federal Reserve bank services covered by the fee schedule shall be available to non-member depository institutions…”.

Unlike some of the more recent scandals at SPDI/crypto banks whose liquidity profile relied on a funding mix that comprised deposits and short-term borrowings to stay afloat, Long has asserted that Custodia’s customer deposits of fiat currency is 100% backed by unencumbered liquid assets, including US currency and Level 1 high-quality liquid assets (HQLA). Under the Basel II Standardised Approach for credit risk, Level 1 HQLA are assigned a 0% risk weight and are the highest quality assets that help banks withstand unexpected cash outflows during market turbulence.

Although some may view Custodia’s pursuance of a master account with the Federal Reserve as pedantic, the move is rooted in Long’s personal experience with the 2011 cyber theft at online bitcoin exchange Mt. Gox, which still ranks as the largest hack in crypto history estimated at USD350 million in financial losses at the time. In June this year, a class action lawsuit will require the now-defunct exchange to pay creditors to the tune of USD9 billion worth of bitcoin.

Custodia’s case against the Federal Reserve is rooted in Long’s assertion that for financial stability, there needs to be a company that can bridge both crypto and traditional banking within the current system. “Custodia offered a safe, federally-regulated, solvent alternative to the reckless speculators and grifters of crypto that penetrated the US banking system, with disastrous results for some banks,” said Long.

The case is seen as a test bed that pushes the boundaries of our current financial system, one in which innovation is forging ahead with no chance for regulators to catch their breath.

Custodia’s motion, however, was dismissed by the Federal Court on 29 March 2024 in favour of the FRB.

Long’s stoic response: “Custodia actively sought federal regulation, going above and beyond all requirements that apply to traditional banks. The board’s denial is unfortunate but consistent with the concerns that Custodia has raised about the Federal Reserve’s handling of its applications, an issue we will continue to litigate.”

In tandem with the rejection, the regulator gave further pushback by releasing a proposed policy to extend crypto-asset restrictions to uninsured state-chartered banks to put them on a level playing field with national banks and federally insured banks.

The regulatory crackdown has continued under the Biden administration. Nicknamed Operation Choke Point 2.0 – a pointed reference to the Obama-era ‘Operation Choke Point’ when high-risk businesses such as gambling operators were cut off from mainstream banking access – the colloquialism has gained traction amongst industry players who view it as an attempt to ‘choke’ them out of accessing mainstream banking services.

Small but high-profile SPDIs like Custodia are unrelentingly pushing back. This August, the financial institution laid off nine of its 36 employees in a bid to preserve capital. Long said: “Operation Choke Point 2.0 has been devastating for the law-abiding US crypto industry and Custodia Bank has been hit hard despite our strong risk management and compliance track record. We are right-sizing so we can maintain operations while preserving capital until after Operation Choke Point 2.0 ends or our Fed lawsuit concludes successfully.”

Although Custodia is the first crypto bank to challenge the Fed for its rejection of the opening of a direct account, others in the digital asset industry aren’t exactly champing at the bit to become members of this highly regulated sector.

What seems to be the biggest bone of contention isn’t so much about the public nature of distributed ledger technology (DLT) as it is about the permissionless aspect of banks holding crypto assets like bitcoin or non-fungible tokens and its impact on financial stability.

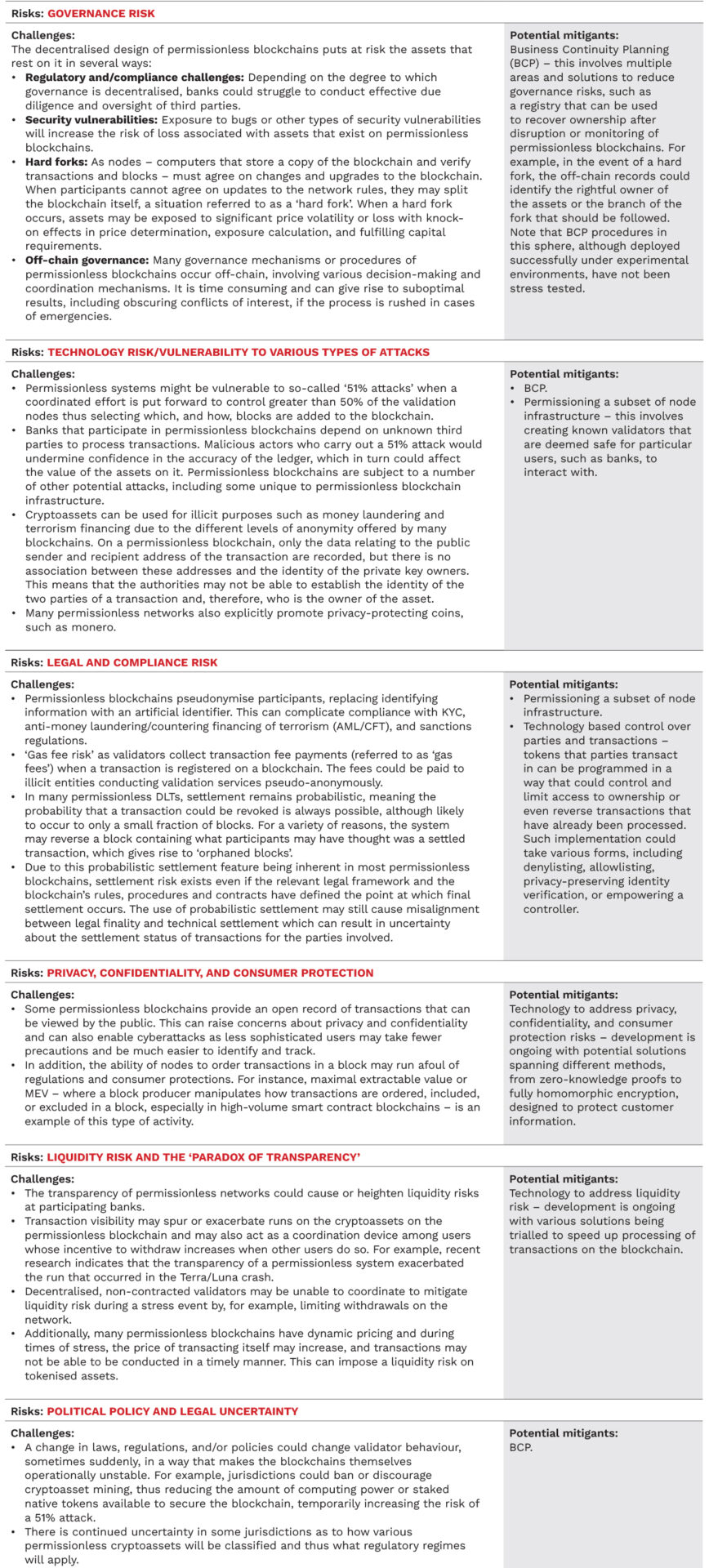

The Basel Committee on Banking Supervision’s (BCBS) most recent thoughts on the matter are captured in its August 2024 working paper titled Novel Risks, Mitigants and Uncertainties with Permissionless Distributed Ledger Technologies, which warns banks of the unique risks posed by technologies in decentralised finance, specifically in relation to cryptoassets which are built on permissionless blockchains.

The latest BCBS research paper outlines known issues, such as the risks of a ‘hard fork’ in the blockchain, lack of oversight over validators, and lack of settlement finality on many DLTs. It explores potential mitigants within the existing financial system and qualifies that none of these have been deployed under real-life circumstances.

Figure 1 gives a condensed version of the major risks, challenges, and potential mitigants for banks according to the global standard setter.

Already, crypto players in advanced markets like the US are proposing that the Securities and Exchange Commission (SEC) adopt a consensus mechanism that would allow it to regulate cryptoassets through simple modifications to existing legislations. Rather than devising new legislation, crypto commentators such as Michael Selig, counsel at a New York-based law firm and expert on crypto regulation, advocate that compromise between innovation and enforcement is the way to go.

Just weeks before the 2024 US presidential elections, Selig writes in an op-ed for cryptocurrency news outlet CoinDesk: “With a change in administration forthcoming, the SEC has an opportunity to institute a hard fork of its own with respect to its approach to crypto regulation. Although legislation is necessary to establish a fulsome legal framework for crypto, the SEC can abandon its regulation-by-enforcement playbook in favour of a pro-innovation regulatory framework that scales to accommodate novel markets.”

Now that the next US president has been decided and we await a second Trump presidency, one market observer who spoke with Banking Insight commented on the possibility of a potential turn-of-the-tides given the greater role that tech leaders and pro-business billionaires are set to play in the administration. “With Elon [Musk] being a major player and now with [Donald] Trump in, there will be greater pressure to adjust,” says the observer.

Logically, the potential workaround which regulators can employ is quite straightforward. Instead of looking at permissionless DLTs, there are several public DLTs that are already permissioned. However, whether they qualify as permissioned under the BCBS’ definition is up in the air; there are also risks associated with its low user base. These include the Inter-American Development Bank’s LACChain and the European Union’s European Blockchain Services Infrastructure.

What is certain is that crypto regulation has reached a hard fork of its own – one in which a concerted resolution by regulators will be needed…and soon. Custodia’s Long portends: “Bitcoin’s going to take a G-SIB (global systemically important bank) down at some point because they don’t understand that the settlement risk is so different between bitcoin and traditional assets.”

With the increased intermingling of investments between traditional and digital asset classes, the question today isn’t whether there will be a ‘safe harbour’ for crypto in banking, but whether banking is safe at all if crypto is not formally brought into the fold.

Angela SP Yap is a multi-award-winning social entrepreneur, author, and financial columnist. She is Director and Founder of Akasaa, a boutique content development and consulting firm. An ex-strategist with Deloitte and former corporate banker, she has also worked in international development with the UNDP and as an elected governor for Amnesty International Malaysia. Angela holds a BSc (Hons) Economics.

Kannan Agarwal is a content analyst and writer at Akasaa, a boutique content development and consulting firm.