Nudging Along: How Behavioural Economics Inspires Product, Pricing & Loyalty

In an increasingly competitive landscape, a different lens brings fresh perspective.

In an increasingly competitive landscape, a different lens brings fresh perspective.

By Kannan Agarwal

By Kannan Agarwal

Are humans rational? Through the lens of behavioural economics, the answer is clearly ‘no’.

In a recent Banking Transformed podcast, Melina Palmer, CEO of The Brainy Business and author of The Truth About Pricing: How to Apply Behavioral Economics so Customers Buy, explains:

“The first and most important thing for everyone to know is to understand how our brains really work because that shows how important it is to be considering psychology. When we look at the way we make decisions, we like to think that the supercomputer in our head is very logical and going by the book for everything all the time and making rational choices about absolutely everything and that we’re in full control of any decisions that we are making.

“In reality, the subconscious is actually making the bulk of decisions that we have at any given time and it’s using rules of thumb, it’s using predictability, it’s using habits to make those decisions. Research has shown that each person makes 35,000 decisions a day on average. When we put it in that context, we realise how many decisions we’re actually making. I love to ask people, ‘How many decisions do you remember making yesterday?’”

The reason why we do not register the bulk of our decisions is because much of our decision-making is done at the subconscious level. “The rules that the brain is using to make decisions,” says Palmer, “is the field of behavioural economics and in behavioural science.”

For many, behavioural economics is currently basking in the sun. Psychologist and Nobel Laureate the late Dr Daniel Kahneman, one of the founding fathers of behavioural economics, upended the premise of rational decision-making in modern economics by proving how neurological human biases lead to irrational decisions. Here are some examples which make up the body of work he jointly developed with Amos Tversky:

Such biases appear more frequently than we would like to admit. The following example, shared by Palmer, shows us that we can work very hard at finding the right answer to a wrong question, but once we see the blind spot, it is possible to use the fundamentals of behavioural economics to correct our course:

Such biases appear more frequently than we would like to admit. The following example, shared by Palmer, shows us that we can work very hard at finding the right answer to a wrong question, but once we see the blind spot, it is possible to use the fundamentals of behavioural economics to correct our course:

“I worked with a credit union on a new rewards checking account. Their billboard said, ‘Earn up to 1.26% APY on up to $25,000 in balances’. That’s math that makes people tune out. I got them to reframe it as: ‘Did your checking account pay you $315 last year?’ They have the same numbers but are completely different. It is easy to say no and creates curiosity to learn more. That simple tweak, even if you didn’t set the rate, gives you a lot of control over what people choose.”

The trick, according to Palmer, is to consciously pivot away from ingrained mental conditioning. “If you don’t spend time really understanding the problem, you build products, add features, and set prices people don’t want, which won’t move the needle. Especially in banking, you are often not your best customer. The curse of knowledge clouds how you think about the outside user experience. Looking for ways to get out of your own way to find what people want is key.”

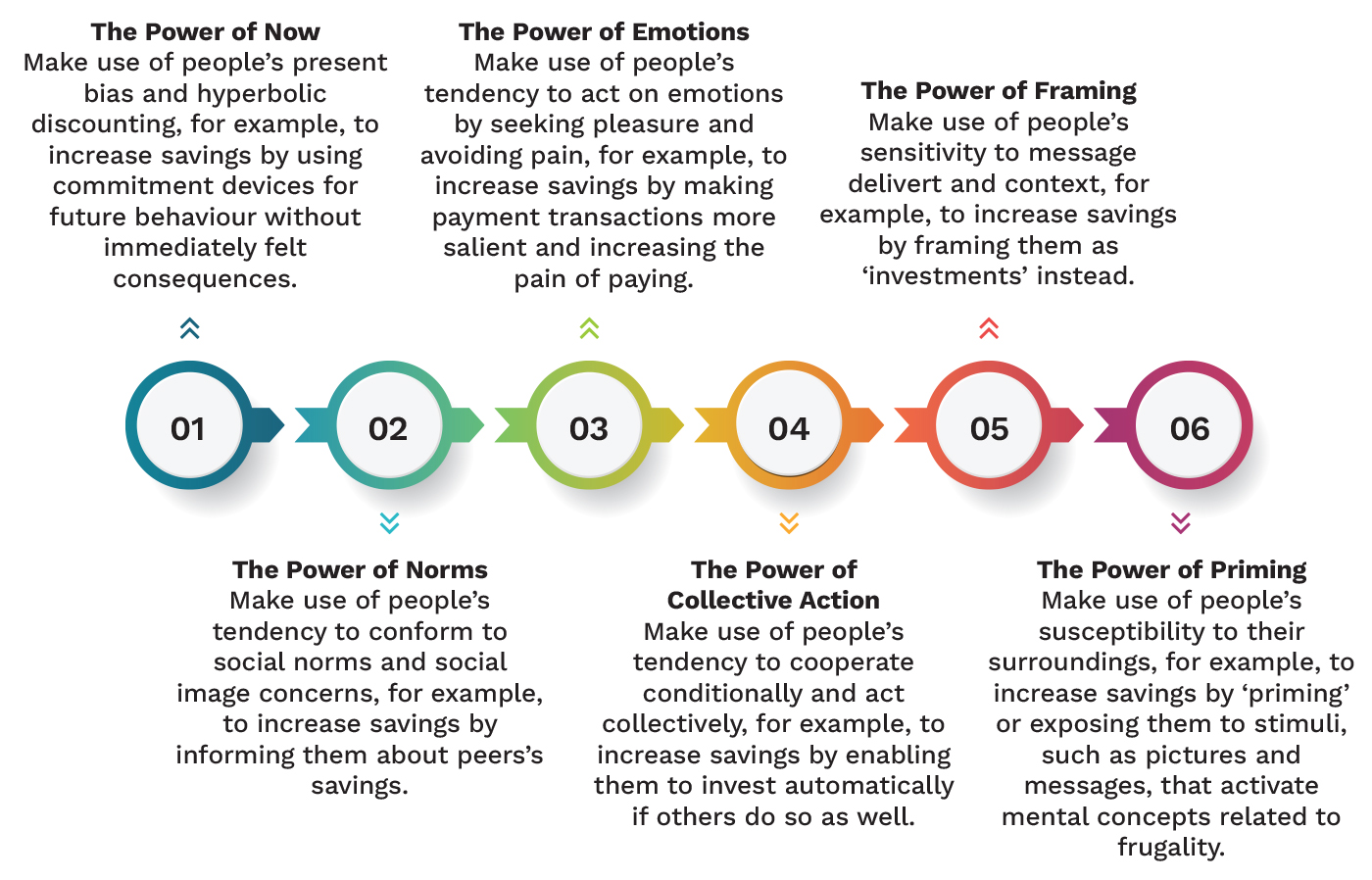

Success requires that banks harness interventions that will break down the behavioural barriers and/or biases of the target demographic without curtailing their freedom to choose. In a recent paper published in The Behavioral Economics Guide 2024 titled From Mindless Consumer to Mindful Citizen: A Behavioral Lens Approach, using the objective of increasing savings (see Figure 1), the authors illustrate how this growing science can be applied to become a game changer for society and financial institutions.

The paper unpacks the mechanics of these ‘nudges’ and how banks can utilise the fundamentals of behavioural economics to influence people towards different (and often, better) life choices. A summary of these six interventions is as follows:

+ The Power of Now. These are interventions that take advantage of opportune times to maximise impact including, but not limited to, incentives and commitment schemes that will increase the propensity of savings plans. Moreover, actions could be based on identifying timely moments when consumers are most receptive to changing their habits and consumption patterns. For instance, banking mobile apps could prompt users with investment opportunities as soon as they receive their salary deposits. The Power of Now actions could seek to incentivise sustainable choices by front-loading benefits (e.g. tax credits that provide immediate savings). For example, the Save More Tomorrow programme, developed by behavioural economists Richard Thaler and Shlomo Benartzi, uses the knowledge of hyperbolic discounting – a cognitive bias where people tend to gravitate towards immediate, smaller rewards instead of delayed, larger rewards – for greater economic good by getting citizens to commit to saving a portion of each future income increase without feeling the pain of saving immediately.

+ The Power of Norms. This makes use of people’s desires or the Power of Norms to drive them towards options that can yield greater financial sustainability and social benefit. It plays on the instinct that most people want to fit in with the various conventions followed by their peers, generation, fellow citizens, or role models. Through awareness and open communication, it is possible to change the social narrative around expectations and nudge people away from a life of excess and high consumption and towards different values, including mindful consumption. Whether through the use of social influencers or harnessing media, this concerted effort to normalise savings and investment programmes can be embedded into popular culture and everyday conversation.

+ The Power of Emotions. Such interventions cultivate the desired behaviour by increasing positive feelings surrounding the end objective, such as increased savings and mindful consumption, whilst also making the negative emotions associated with the opposite objective more prominent. This can come in many forms and should be a two-pronged approach in order to obtain its maximum effectiveness. When people indulge in the desired target behaviour, there must be a systematic process which affirms the feel-good factor as well as a process to supplant any feelings of inadequacy in individuals who choose to go ‘against the grain’. For instance, to strengthen negative emotions associated with mindless spending, the financial impact of spending in general can be made more salient. For example, a Swiss smartphone app used an emotion-based approach to highlight credit card transactions, making users more mindful of cashless spending.

+ The Power of Collective Action. People’s actions as consumers often lean toward selfishness. To counter this, mechanisms for conditional cooperation and collective action can help. For example, in the context of offsetting CO2 emissions, instead of offering people the opportunity to pay to offset their individual emissions, the offer could instead be a call to action – the chance to offset carbon emissions can happen only if enough people collectively do so.

+ The Power of Framing. Framing, or how a message is presented, is known to cause large differences in people’s reactions to a message. Leading research from the Behavioural Insights Team has shown how reframing ‘savings’ as ‘investments’ was found to increase suggested pension savings by 33% among young people. Using this knowledge to reframe certain messages or change how people think about specific choices can lead to vastly different outcomes. Thus, reframing can be used to change people’s perspectives and affect their choices as a result.

+ The Power of Priming. Priming, or exposing people to a stimulus to temporarily activate specific mental concepts, can be an effective way to influence people’s behaviour in a passive or even hidden manner. For example, research has found that exposure to art leads to less interest in status-oriented consumption by inducing a more meaningful, deeper state of transcendence.

Coming back to her point, Palmer concludes that there are “many paths with those 35,000 decisions going different ways…understanding how time matters to people is one.”

“We’re all victims to time discounting,” she says, “what I call the ‘I’ll Start Monday’ effect. Setting the alarm to run and then hitting snooze. We think of our future selves like a different person…bringing it to the now can be impactful.”

Whatever their tools of choice, the end goal is for financial institutions to use the power of behavioural economics to drive future behaviour. Whether it is through more responsive ways of rate-setting or manipulating subconscious behaviours towards more sustainable choices, bankers must feel that they are psychologically empowered to approach these time-old problems in new and innovative ways.

Kannan Agarwal is a content analyst and writer at Akasaa, a boutique content development and consulting firm.