Sustainability of Our Own Accord

The BCBS’ voluntary framework adds granularity to IFRS compliance.

The BCBS’ voluntary framework adds granularity to IFRS compliance.

By Julia Chong

By Julia Chong

Navigating the increasingly complex matrix of environmental, social, and governance (ESG) reporting has never been more urgent for financial institutions. The good news is that the banking sector in some jurisdictions in Asia are already well-placed to syncretise these standards at both the national and international levels.

Right off the bat, Malaysia had adopted a hybrid reporting standard for its ESG reporting. This was in line with standard-setters’ expectations that local entities cast their eyes simultaneously on national-specific and international benchmarks.

Locally, financial institutions are guided by Bank Negara Malaysia’s National Sustainability Reporting Framework (NSRF), which was announced in September 2024. The NSRF requires entities to “produce consistent and comparable disclosures to enhance the credibility of the reports and promote improved decision-making and stakeholder engagement”.

Based on the NSRF, the central bank has set a phased-in timeline beginning 2025 for the financial sector to produce climate-related disclosures that are aligned to the International Sustainability Standards Board’s (ISSB) International Financial Reporting Standards’ (IFRS) S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and IFRS S2 (Climate-related Disclosures). More importantly, the ISSB standards are developed in line with the recommendations of the global Task Force on Climate-related Financial Disclosures, ensuring that IFRS S1 and S2 compliance forms the baseline for ESG reporting standards.

Moving forward, IFRS S3 (Biodiversity, Ecosystems and Ecosystem Services), currently in the research and consultation stage, will integrate biodiversity risk into financial reporting alongside traditional financial metrics.

It is no surprise then that the market’s reaction to the Basel Committee on Banking Supervision’s (BCBS) latest guidance on climate-related disclosures, A Framework for the Voluntary Disclosure of Climate-related Financial Risks (Framework), is lukewarm as foreign markets gravitate toward deregulation of the banking sector.

Released this June, the Framework is an extension of the BCBS’ consultation with market players conducted in late 2023 to explore how a Pillar 3 disclosure framework would strengthen the regulation, supervision, and practices of banks for enhanced financial stability. The BCBS has expressly stated that implementation of the Framework, which includes templates to build consistent climate risk data, is flexible and it is left to national supervisory authorities on whether to integrate it nationally.

It is clear that the BCBS’ voluntary Framework complements – not replaces – the ISSB standards in several ways:

It is necessary then that the Framework is viewed as a complementary tool for banks which can reduce information asymmetry, ambiguity, and deliver more impactful reporting in the ever-expanding IFRS sustainability standards.

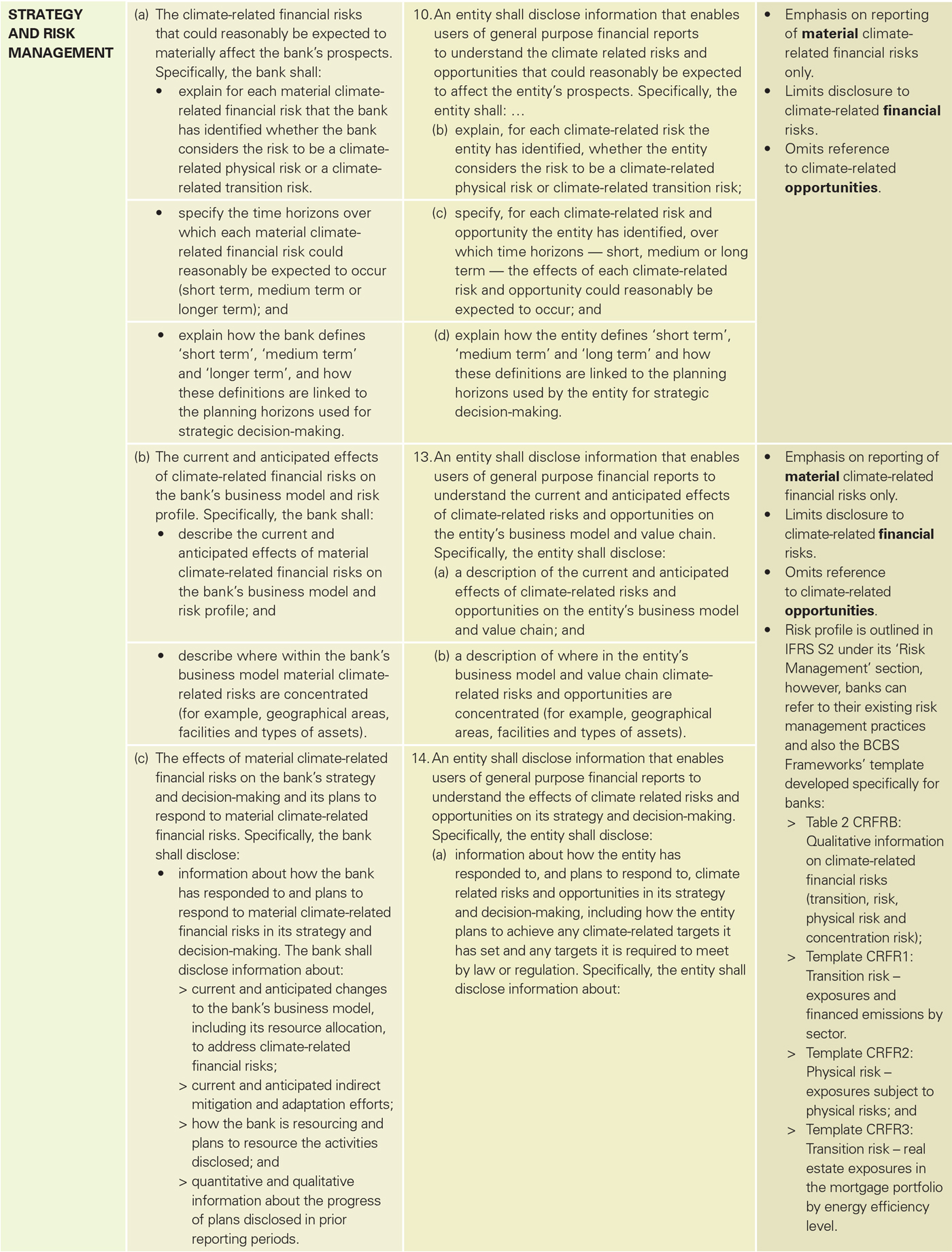

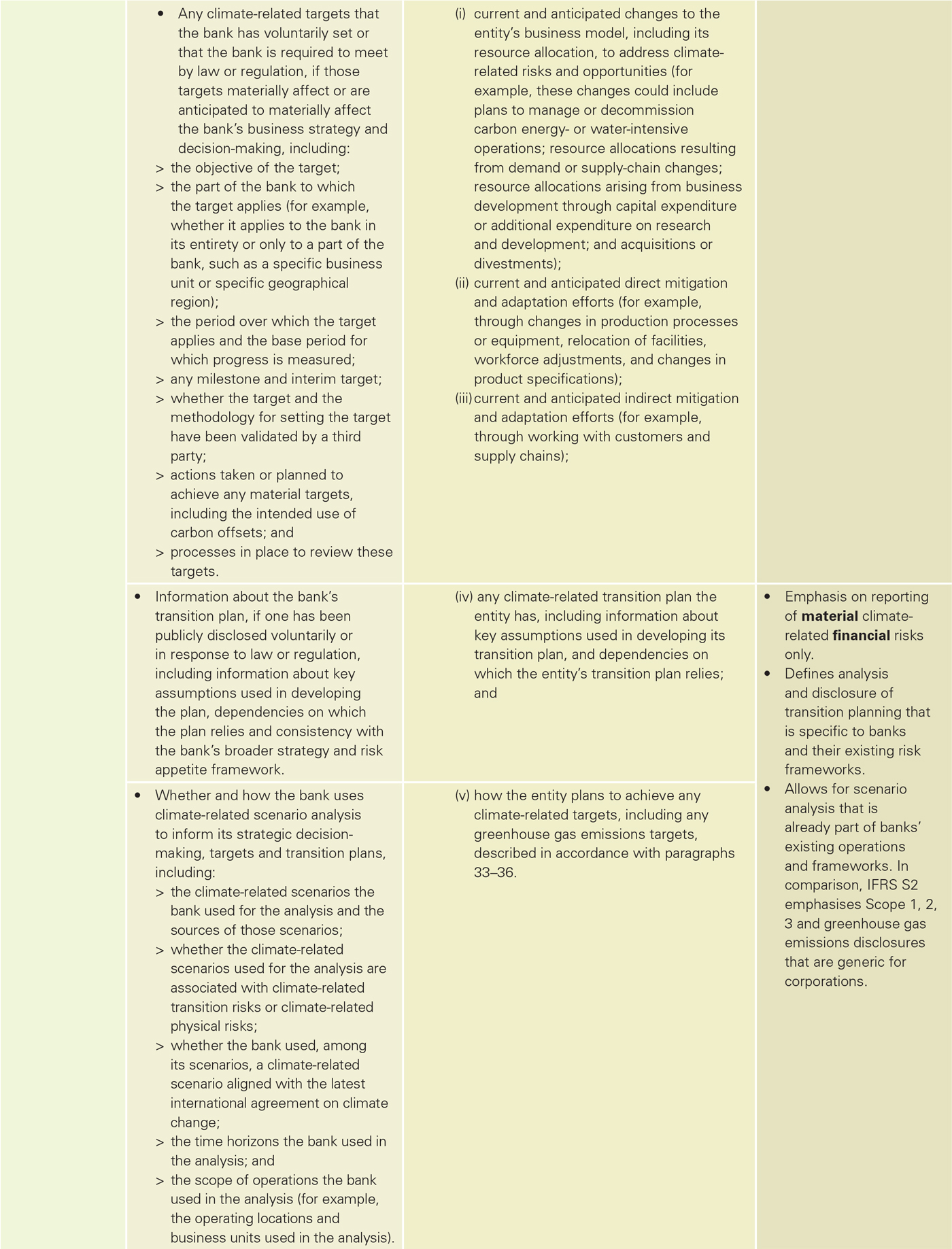

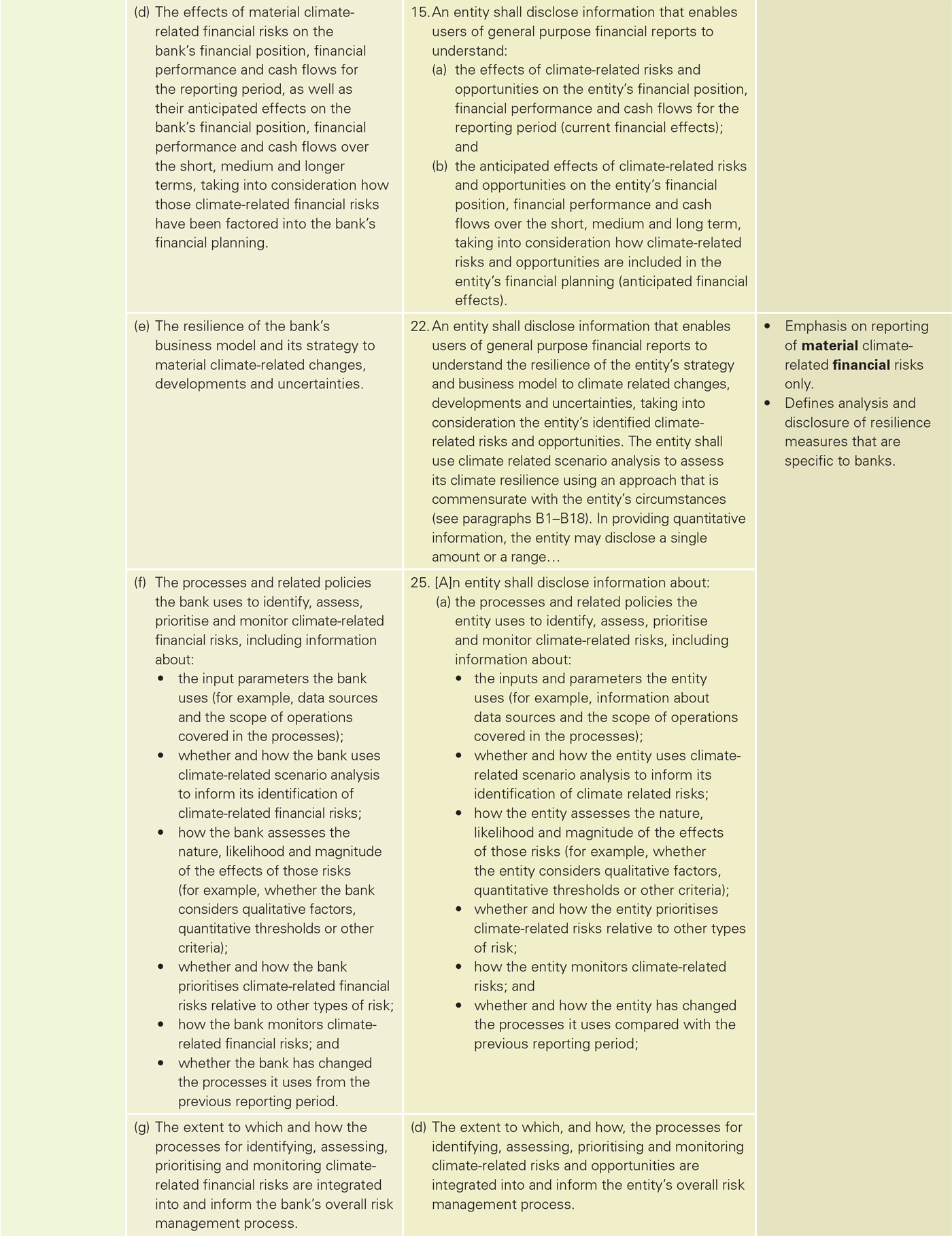

To illustrate this, Figure 1 is a comparison between the minutiae of the Framework and IFRS S2, which will be useful to banks in two ways: (i) the Framework’s simplified and granular data requirements lessen the ‘grey areas’ when reporting quantitative, qualitative, transition, and physical risks in finance; (ii) it signals regulatory expectations in the near and medium terms for banks.

At a time when the US, UK and Europe are pushing back against a rules-based regime, it is crucial that Asian banks hold their higher ground against destabilising elements.

Here is our comparative analysis of how the BCBS Framework can reduce ambiguity and information asymmetry for banks that are already benchmarking their sustainability reporting to the IFRS’ S1 and S2.

Julia Chong writes for Akasaa, a strategic consulting and publishing firm with offices in London, Sharjah, and Kuala Lumpur.