Battle for ‘Woke Banking’

Asia leads on how the financial sector balances climate commitments with market realities.

Asia leads on how the financial sector balances climate commitments with market realities.

By Angela SP Yap

Remember the proverb, ’when the going gets tough, the tough get going’?

Well, sometimes, when things get tough, some of us just…go.

Since December 2025, some of the world’s largest financial firms have explicitly opted out of the net-zero agenda, reversing the momentum of the sustainability finance movement and bringing crucial coalitions to their knees.

In March 2025, a Bloomberg Green analysis found that ‘green chatter’ – the use of words like ‘climate’ and ‘sustainability’ – among S&P 500 companies plunged by 76% after Donald Trump came to power again and pulled out of the Paris Agreement a second time. ‘Greenhushing’ is now an entrenched term and US companies actively flag climate terms among words to avoid in their earnings calls.

The series of departures by financial institutions in America, Canada, the EU and Japan from important finance-led climate-change initiatives reads like a ‘who’s who’ of financialdom. These high-profile withdrawals signal the growing tension between practical commitments to climate action and geopolitical pressures.

But let’s be frank. The writing was on the wall long before this exodus.

As early as 2022, we raised the red flag when the world’s biggest finance-led climate-change initiative, the Glasgow Financial Alliance for Net Zero (GFANZ) quit the United Nations’ Race to Zero (RtZ) campaign. This marked the first major blow to the climate finance movement.

In Banking Insight’s December 2022 cover story, Will the Adults in the Room Please Stand Up, I wrote that this was “a crucial adulting moment for banks” who needed to send a clear signal and step up to combat climate finance myopia. Sadly, this was not the case.

GFANZ is the umbrella global finance pact started by Mark Carney, the former Bank of England Governor and now Prime Minister of Canada. Its objective was to assist banks in reducing their carbon footprint and help borrowers transition from brown to green economies. GFANZ’s premature withdrawal from the RtZ showed the world how rocky the road is for transition finance.

Last year’s fallout began when Republican representatives under the Trump administration introduced over 100 new legislative bills to penalise pro-ESG (environmental, social, and governance) practices and said membership with GFANZ-backed organisations could breach US antitrust laws.

Goldman Sachs was the first to announce in December 2024 when it quit the Net-Zero Banking Alliance (NZBA), one of the biggest industry-specific associations under GFANZ. This triggered a slew of other banks – JP Morgan, Citigroup, Bank of America, Morgan Stanley, RBC, ScotiaBank, HSBC, UBS, Mizuho, Macquarie – to follow suit. With over 140 banks representing a collective USD49 trillion in assets, NZBA had pledged to eliminate lending and investments into carbon-intensive sectors by 2050. By October 2025, the dream was over. NZBA ceased operations after its members voted to dissolve the coalition.

Concurrently, in January 2025, the Net Zero Asset Managers (NZAM), another GFANZ-led initiative comprising over 325 asset managers with USD7.5 trillion worth of assets under management, suspended its operations after a series of high-profile exited from its membership.

The shock announcement of the suspension was explained in its press release: “Recent developments in the US and different regulatory and client expectations in investors’ respective jurisdictions have led to NZAM launching a review of the initiative to ensure NZAM remains fit for purpose in the new global context. Signatories will be consulted throughout the review process and informed of any updates in a timely and transparent fashion.

“As the initiative undergoes this review, it is suspending activities to track signatory implementation and reporting. NZAM will also remove the commitment statement and list of NZAM signatories from its website, as well as their targets and related case studies, pending the outcome of the review.”

Meanwhile, Asian banks have held on to the Paris Agreement pledge and continue to support the climate financing agenda.

In Malaysia, Bank Negara Malaysia reports that its banks have doubled-down on their ESG financing, pledging over MYR240 billion for green and transition activities up to 2027, a MYR130 billion increase from the year prior.

Across the straits, Singapore banks have reported upticks in their 2025 ESG loan portfolios, with DBS increasing its sustainable financing commitments to SGD102 billion (+SGD13 billion) and OCBC at SGD80 billion (+9 billion year-on-year).

The biggest lenders in Asia-Pacific are also investing in new research and in-house models to assess sustainability related risks and opportunities – such as force majeure and impact investing – in line with guidelines from global standard-setters.

Much of this work is in collaboration with internationally ranked universities in the UK, multilateral lenders like the World Bank, and international development agencies such as the United Nations Development Programme.

These reflect the growing sophistication in Asian banking to meet the world’s future challenges head on. It stands in stark contrast to the policy rollbacks that have been coming out of Wall Street and its posse of late.

How will these battling interests impact sustainable financing?

In February 2026, NZAM announced its comeback with an updated roll call of 254 members, down significantly from its 331-member roster at the start of last year. Unsurprisingly, the biggest US banks and fund managers were visibly missing, a clear sign that the government of the day is still digging its heels deep into the anti-ESG agenda.

They aren’t the only ones. Countries such as New Zealand are also tussling with the same opposition to sustainable finance. The island nation’s New Zealand First, a right-wing populist political party led by Winston Peters, recently introduced a Member’s Bill in parliament to fight ‘woke banks’, preventing lenders from refusing services to businesses based on the current ESG framework.

Popularly dubbed the ‘Woke Banking Bill’, his use of ‘woke’ to describe ESG-aligned policies in banking is intentional.

‘Woke banking’ is a pejorative term that refers to the values of sustainability finance – all 17 of the United Nations’ Sustainable Development Goals. From climate action and gender equality to innovation and sustainable cities.

Rooted in African American culture, ‘being woke’ once meant that one has awakened to systemic injustices – racism, inequality, and other forms of discrimination. But the term has evolved. If someone calls you ‘woke’ today, they’re likely mocking you for behaving morally superior, a liberal who spoils it for everyone else.

That is what Peters means when he opines: “This Bill ensures fairness and prevents ESG standards from perpetuating woke ideology in the banking sector being driven by unelected, globalist, climate radicals.”

He was adamant that the proposed amendment to the nation’s Financial Markets Act 2022 would “remove the ESG Framework’s stranglehold on corporations” and “stop banks imposing woke-riddled, expensive, deadweight costs on our productive sector” A financial institution that contravenes this is liable, upon conviction, to a prison term of up to three months or fine not exceeding NZD50,000 for individuals; and a fine not exceeding NZD500,000 for companies.

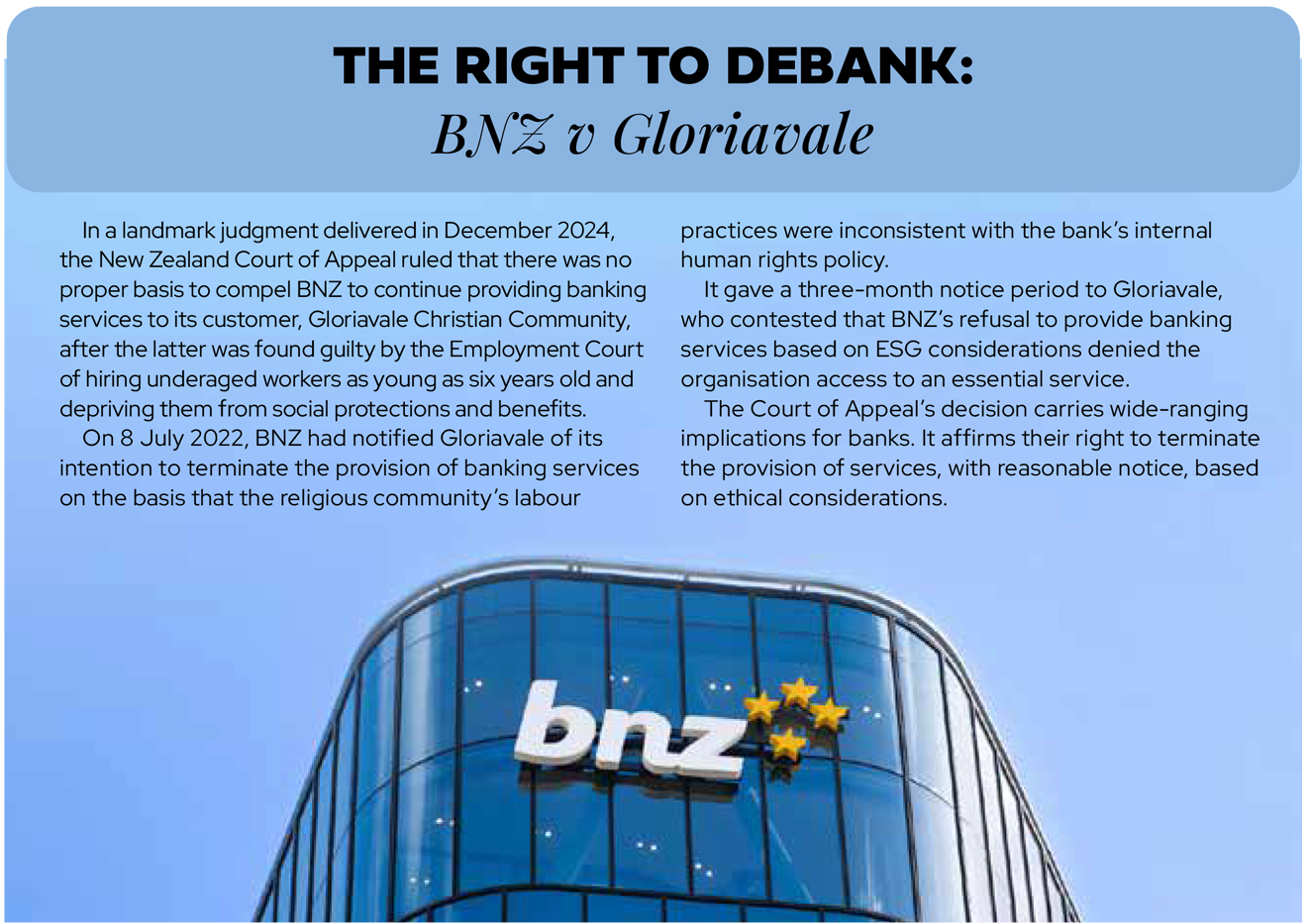

Much of this backlash was sparked by a December 2024 judgment by the island country’s Court of Appeal in the landmark ruling, Bank of New Zealand (BNZ) v Gloriavale. Read The Right to Debank on page 22.

The explanatory notes to the proposed Bill state: “This amendment is intended to prevent registered banks ‘debanking’ or withdrawing banking services from New Zealanders, body corporates or companies, whose political views or outlook may not align with the sensibilities of that institution. This includes the withdrawal or refusal to provide banking facilities and services from businesses on murky ‘environmental, social, or governance’ moralising.”

Simply put, we’re tired of virtues. Let’s get back to ‘drill baby, drill’.

When tabled in parliament this May, New Zealand’s Finance & Expenditure Select Committee rejected the proposed Bill with 59% of lawmakers opposing it. What about the 41% who didn’t?Just as there are no eternal friends or enemies, there doesn’t seem to be a clear frontrunner in this ideological tussle within sustainable finance.

In the pursuit of a win, let’s hope humanity doesn’t end up being the biggest loser.

Angela SP Yap is a multi-award-winning strategist and social entrepreneur championing Asian perspectives in global conversations. Through her editorial consulting firm, Akasaa, she transforms regional insights into compelling narratives that bridge business, policy, and culture – shaping industry discourse with a distinctly Asian lens grounded in economic analysis and cross-sector expertise.