Recycling Risk or Risking Resilience?

A deep dive into the increased uptake of SRTs and what it means for the financial system.

A deep dive into the increased uptake of SRTs and what it means for the financial system.

By Julia Chong

With some of the biggest non-bank financial intermediary blow-ups in 2025, private credit as the newest asset class on the block has dominated headlines. Meanwhile, another growing (and slightly related) asset class has been quietly brewing on the backburner.

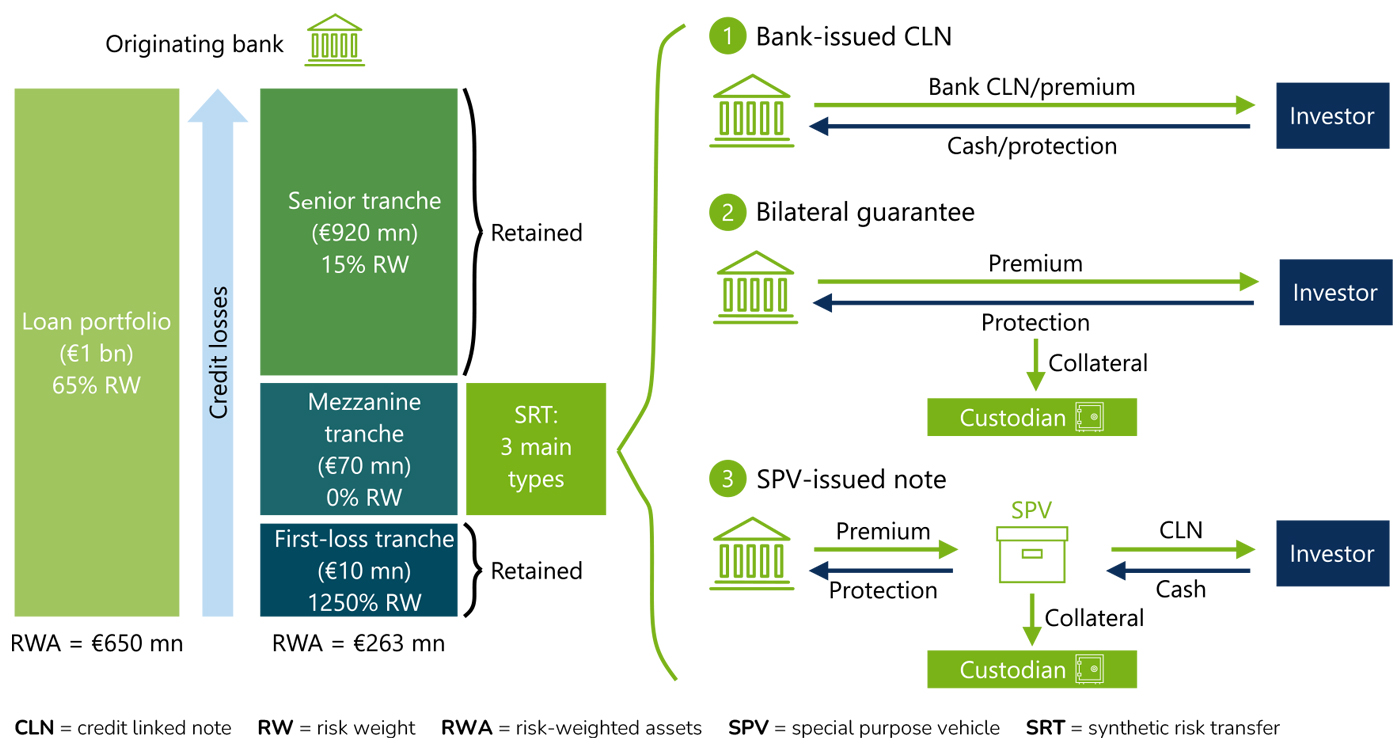

Synthetic risk transfers or SRTs have flourished from a niche securitisation instrument into a serious contender for banks seeking to redistribute their risks yet maintaining ownership of these assets in their portfolio.

Tanuj Khosla, senior trader for global markets, at Louis Dreyfus Company explains how banks put SRTs to good use in an issue of The Asset: “Put simply, SRT refers to a financial transaction in which credit risk is transferred without selling the actual assets, typically through the use of credit derivatives.

“Banks do SRTs primarily for capital relief. By transferring risk, banks reduce RWAs (risk-weighted assets), which in turn lowers capital requirements under Basel III and IV. This freed-up capital can then be used to create new loans, which can improve a bank’s return on equity. Even from a risk management perspective, SRTs help banks manage concentration risk or sector/geography exposure.

“Banks facilitate SRTs mostly via a credit default swap (CDS). A bank retains the loans on its balance sheet but purchases credit protection on a specified tranche of losses. Investors get premiums in exchange for taking on the risk of first losses. These investors are mostly hedge funds, private credit funds and insurers who are looking for uncorrelated returns and trying to get some ‘free money’ without posting any capital.”

From the emergence of bespoke credit in the 1990s to the notorious collapse of CDS’ which triggered the Global Financial Crisis (GFC) in 2008, the SRT market grew by 241% between 2020 and 2024, measured by issued volume. Synthetic securitisation volumes have grown from EUR55 billion in 2016 to EUR260 billion in 2024 and some market estimates have pegged that outstanding SRT loans currently stand within the range of EUR1 trillion.

Historically, the SRT market has primarily been dominated by EU banks and comprised mostly of corporate loans. This investment profile has changed in recent times.

Today, although EU-domiciled and American-based banks still make up a significant portion of new global deals, Asian banks are ramping up as they rely more on NBFIs for credit protection and risk diversification. See Asian Deal Book on page 77.

The SRT pool size remains modest in comparison to banks’ capital and risk-weighted assets. Of greater concern is how quickly it is becoming embedded as a tool for strategic portfolio redistribution within global systematically important banks. Here’s why.

Like all other forms of securitisation, the structure of each SRT – underlying assets, transaction types, tranches, etc. – is largely driven by the capital relief that can be obtained under the relevant national capital requirement rules and/or other considerations like investor funding and regulatory approvals.

For instance, the SRTs are generally structured by banks to equal or exceed the maturity profile of the underlying loans – this puts to rest the issue of a tenure or funding mismatch. The size of the issuance also matters – smaller tranches with stretched-out maturity dates will also reduce the risk of the SRT for banks. Then there is the diversity of its investor base – a rule of thumb is that the less concentrated the SRT investor base is, the more spread out the risk appetite and financing conditions are because of the wider investor pool. These determinants drive issuance volumes and pricing.

Regulatory rules and market uptake also vary between jurisdictions and economic regions.

For instance, the Monetary Authority of Singapore has signalled that Singapore banks may only utilise SRTs for capital optimisation, flexibility, and portfolio steering – not as what some have termed a “big bang capital tool”.

In December 2025, the European Central Bank (ECB) announced the availability of an SRT fast-track process, which would reduce approval time from three months to two weeks. The option is available only when certain conditions are met by the bank: (i) when the securitised portfolio is performing, not concentrated, and does not contain more than 20% of leveraged loans; (ii) when the impact on the bank’s capital ratios of the significant risk transfer is lower than 25 basis points; (iii) when standardised contractual early termination clauses are used. Increased ECB-led micro- and macroprudential scrutiny should be expected as another precautionary route to discourage undue risk-taking and minimise impact on systemic resilience.

Recent geoeconomic instabilities have not materially impacted deal volumes and sizes in the SRT market. It is more from a financial resilience perspective, that the SRT market poses potential emerging risks that could unseat the banking sector, according to the BIS’ Quarterly Review released this March:

+ Rollover or flowback risk: Some supervisory authorities such as the UK Prudential Regulation Authority have stated the need to incorporate flowback risks into bank capital planning frameworks, whilst others like the Finansinspektionen, Sweden’s financial regulator, have developed methodologies to assess and mitigate it. Others such as the US and EU have relaxed.

+ Investor leverage and liquidity risks: Although this appears to be modest and contained, theoretically, leverage can lead to forced asset sales in times of stress. Anecdotal evidence also indicates that there is a liquidity mismatch among SRT investors albeit limited, as many SRT funds use closed-end structures that allow them to manage redemptions without having to sell holdings. For open-ended funds, they deploy either an evergreen structure less exposed to redemptions, allocate a small fraction of their multi-asset portfolios to SRTs or manage redemptions through bank lines and internal liquidity buffers.

+ Interlinkages and risk transfer chains: Hidden vulnerabilities are cause for concern in increasingly complex risk transfer chains amongst SRT market participants. This is more pronounced during times of stress. One example is the ‘circles of risk’, where credit risk transferred from banks to funds via SRTs can return indirectly to the banking sector as a result of other banks financing the purchase of those investors. Repackaging of SRT exposures adds further layers of complexity which can, in principle, recreate pre-GFC-type amplification mechanisms. Opacity surrounding investor characteristics, cross-border exposures, and funding links limit the authorities’ ability to monitor concentrations, leverage, and interconnectedness – possibly until it is too late.

+ Growing interconnectedness between banks and non-bank financial institutions (NBFIs) could result in a scenario where SRTs could contribute to a procyclical tightening of bank lending capacity, which would then enhance bank-NBFI adverse feedback loops.

Prospects are that SRT numbers by volume and issuance size will increase in Asia Pacific. Investors – credit funds and asset managers alike – will view it as an opportunity to access high-quality Asian corporate loans managed by strong regional banking groups. What remains is the institutional controls that must be in place to ensure systemic risk and financial resilience are not compromised.

Julia Chong writes for Akasaa, a strategic consultancy and publishing firm. From its bases in London, Kuala Lumpur, and Sharjah, it delivers Asia-informed insight to a global audience.