Why Banks Should Bet on Empathy

Listening pays off in the long run.

By Marjorie Giles

In 2020, Accenture conducted a global study comprising 125 senior executives from the top five banks. The subject was Empathetic Banking. A questionnaire was devised to identify these leaders as either Empathetic Banking Leaders, Contenders, or Laggards. Their answers were then compared against the banks’ self-reported non-financial performance metrics (customer loyalty, newly acquired customers, customer trust, employee engagement scores, employee productivity, and customer cost-to-serve) and, finally, plotted against their financial performance.

The objective was to quantify how much of a role customer-directed empathy had played in their service model and had they seen the returns of their investment in this new approach.

The results, captured in the firm’s 2021 report titled Banking on Empathy: Engaging with Customers in a More Human Way, showed that banks led by Empathetic Banking Leaders – individuals with strong capabilities for understanding and responding appropriately to a customers’ emotional state – financially outperformed their peers and increased revenue by 1.3%, whilst Empathetic Banking Laggards saw revenues contract by 0.6% on average.

Researchers deem empathy to be a personality trait defined as “the ability to identify and understand another person’s feelings, thoughts and situation”, categorising it into two types: cognitive and affective.

Cognitive empathy, also known as ‘perspective taking’, is the ability to step out and look at the situation from the other person’s point of view. High cognitive empathy means that a person can ‘read’ another person’s needs and intentions based on verbal and non-verbal cues and takes actions to address the issue.

Affective empathy, however, is more emotion-laden. The individual responds to the other person’s emotional state without having experienced the emotion themselves. This induces feelings of concern but also contagion, where one mimics the other person’s gestures or experiences stress when the other person is fearful or anxious.

In the business world, many see empathy as a disadvantage, an indication that you are just not cut out for the job. However, numerous studies in marketing and sales literature point to just the opposite: the best salespeople are also the most empathetic listeners.

Research proves that empathy is a predictor of trust and determines the quality of their relationship with the financial institution. In the customer’s eyes, the question, “Do I trust my banker?” is nearly indistinguishable from “Do I trust my bank?”. Studies, such as one published in the International Journal of Bank Marketing by Omar S Itani and Aniefre Eddie Inyang from the University of Arlington, Texas, reinforce why banks should never underestimate the power of the personal touch, something which digitalisation cannot fully replace. Their 2016 paper, The Effects of Empathy and Listening of Salespeople on Relationship Quality in the Retail Banking Industry, posits that “empathy and listening have been found to be important determinants of customer satisfaction and, thus, relationship quality (RQ). The objective is to examine the relationship between a bank’s salespeople’s empathy and listening, and the customers’ RQ with the bank from the perspective of the customers.”

The authors posit that exhibited empathy by retail banks’ salespeople raises the RQ between customer and the bank: “When salespeople practice effective listening skills, they are more likely able to accurately assess verbal and non-verbal cues from their customers and to respond appropriately, enabling them to build rapport with customers”.

“[Lucette B] Comer and [Tanya] Drollinger [in their 1999 paper Active Empathetic Listening and Selling Success: A Conceptual Framework published in the Journal of Personal Selling & Sales Management] found that salespeople with effective listening skills can “develop and maintain long-term relationships with their customers”. They also found that effective listening skills lead to an increase in customer satisfaction. Customer satisfaction with a salesperson after an interaction is based on an emotional state in which the customer assesses the quality of the interaction experience. Therefore, when customers perceive the salesperson as having effective listening skills, they are likely to have a positive assessment of the interaction with the salesperson.

Whether it is anticipating a customer’s need when making a financial decision or making account holders feel that their opinions matter (a feeling that’s increasingly lost in the ‘noise’ of remote banking), it pays for financial institutions to invest in upping the emotional quotient of their workforce.

Itani and Inyang suggest some ways to achieve satisfaction:

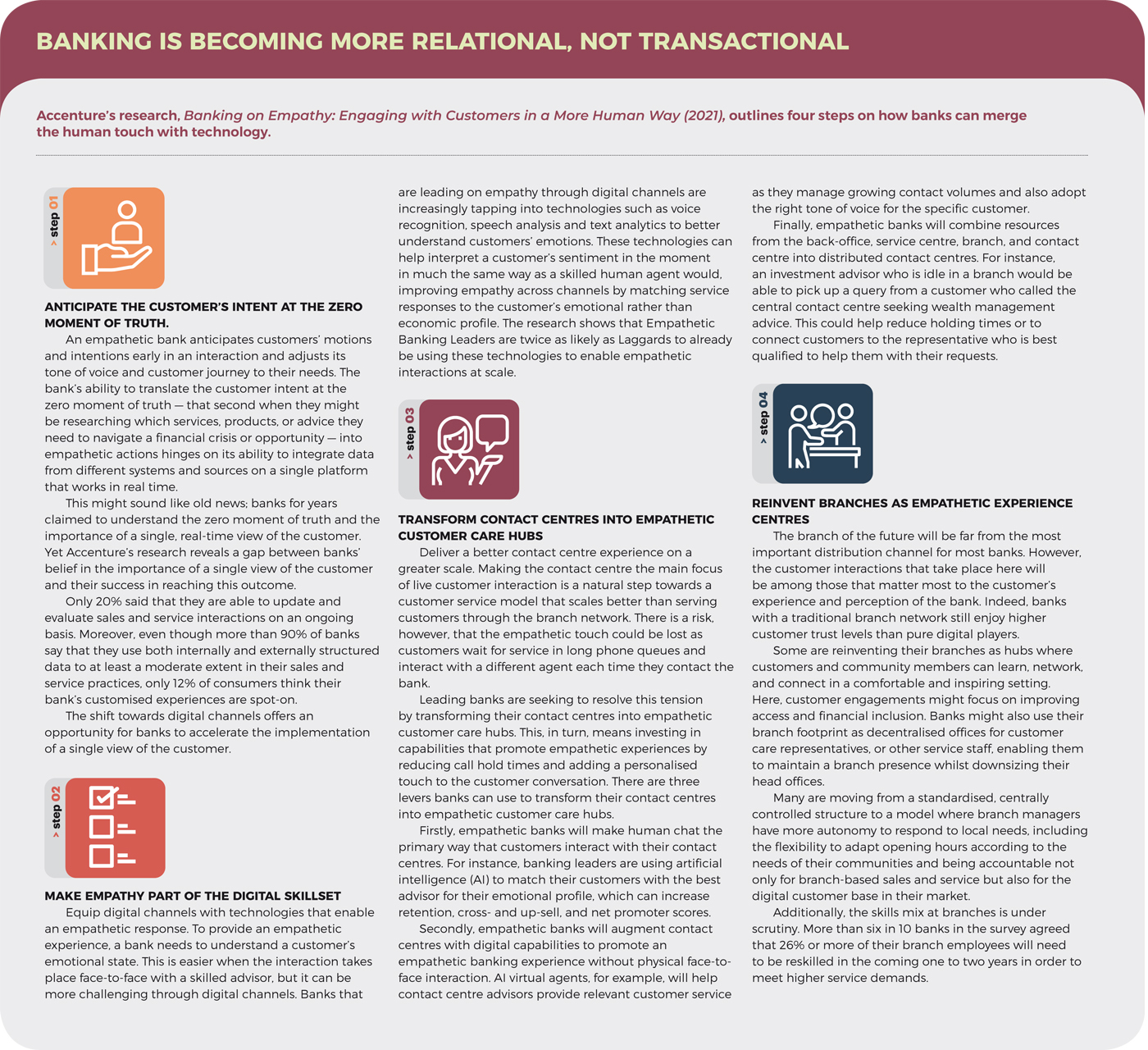

The digitalisation of the banking sector should not be seen as separate from empathetic banking. In fact, it is imperative to acknowledge that the technological tools at our disposal – artificial intelligence, virtual reality, speech analytics, and other tools – cannot supplant human intuition, but can be deployed to assist bankers in making the customer journey more intuitive and emotionally satisfying.

Marjorie Giles writes for Akasaa, a boutique content development and consulting firm, and holds a Masters in Clinical Psychology.