The Journey Towards Frictionless Cross-Border Payments in APAC

Delve into the aspirations for a frictionless cross-border payment landscape.

Delve into the aspirations for a frictionless cross-border payment landscape.

By LexisNexis Risk Solutions

By LexisNexis Risk Solutions

Cross-border payments in the Asia-Pacific (APAC) region have traditionally been characterised by inefficiencies, high costs, and varying levels of transparency. According to an article by The Payments Association, 55% of firms lose 4%–5% of revenue per month due to manual tracking and reconciling transactions. These challenges have been exacerbated by disparate regulatory frameworks and the complexity of international transactions. While there are significant advancements in domestic payments across the APAC region, similar advancements in cross-border payments have been slow.

Improving cross-border payment systems is crucial for fostering economic growth, promoting international trade, and enhancing financial inclusion. A more efficient and seamless payment infrastructure can reduce transaction costs, mitigate risks, and improve overall economic stability throughout the APAC region.

The ideal vision for cross-border payments in the APAC region involves instant, cost-effective, and transparent transactions, mirroring the ease of domestic payments. This aspiration includes:

While the ideal vision is to mirror the process of instant payment in the cross-border payments journey, the practical reality for individual regions is to work around the key cross-border challenges. These include:

These are the roles of each stakeholder:

+ Traditional financial institutions play a crucial role in providing the infrastructure and trust needed for cross-border transactions. Their extensive networks and regulatory compliance capabilities are vital in ensuring secure and reliable payment processes. They are expected to continue playing a key role as fintech companies use the infrastructure and compliance rails to enable cross-border payments.

+ While traditional financial institutions form the backbone of payment services, fintech companies are likely to be at the forefront of innovation, driving the development of new technologies and solutions that enhance the efficiency and user experience of cross-border payments. They are instrumental in bridging gaps in traditional banking systems and providing alternative payment methods.

+ Governments are key in establishing regulatory frameworks that facilitate cross-border payments while ensuring security and compliance. Their role varies by country, with some focusing on fostering innovation through supportive regulations and others emphasising stringent security measures. In cross-border payments, however, it becomes tougher to enforce common formats and enable interoperability in payments messages. ISO 20022 has in some way created a common messaging structures across the globe, however, governments need to drive regulation within domestic payments systems to drive error-free instant payments across borders. The government’s aim to drive regional economic growth will help shape localised standards and interoperability within cross-border instant payment systems.

Countries across the APAC region are adopting different approaches to cross-border payments. Some are focusing on instant account-to-account payments, while others are developing closed-loop systems that dominate their domestic landscapes. The panel sees potential for greater regional convergence through:

Understanding the current payment landscape requires a look at its evolution. The past decade has seen significant advancements in digital payments, driven by technological innovation and changing consumer behaviours. The present focus is on enhancing interoperability, reducing transaction costs, and improving user experiences. The desired future state is one where cross-border payments are indistinguishable from domestic transactions in terms of speed, cost, and convenience.

The payment roundtable also discussed various key trends currently shaping the industry. Some of key trends identified included:

Main discussion points of top key trends identified from the above:

+ Interoperability between systems

Achieving interoperability between different payment systems and across jurisdictions remains a significant challenge. Standardising protocols and enhancing connectivity are essential for facilitating seamless cross-border transactions. Where standardisation is not achievable, a tactical interoperable translation of payment information and instructions can enable error-free cross-border transactions. In this regard, having both source and destination payment data is key in such transactions.

+ Regulatory compliance across jurisdictions

Navigating diverse regulatory requirements across multiple jurisdictions adds complexity and cost to cross-border payments. Harmonising regulations and promoting cross-border cooperation are essential for simplifying, reducing compliance burdens, and enhancing efficiency within payments.

+ Managing fraud and security risks

Cross-border payments are vulnerable to fraud and cybersecurity threats due to the global nature of transactions. Implementing robust security measures, real-time monitoring systems, and enhanced authentication protocols are critical to mitigating risks and safeguarding transaction integrity.

+ Cost and transparency issues

High transaction fees, hidden costs, and opaque exchange rates are common concerns for users of cross-border payment services. Improving cost transparency and reducing transaction fees through competitive pricing and innovative solutions can enhance customer trust and satisfaction.

+ User experience and friction

Complex payment processes, long settlement times, and cumbersome documentation requirements contribute to poor user experiences in cross-border payments. Streamlining procedures, enhancing user interfaces, and providing real-time transaction tracking are essential for improving customer satisfaction.

The development towards frictionless cross-border payments carries risks such as increased exposure to fraud. However, from a risk-benefit assessment, the benefits of improved efficiency, reduced costs, and enhanced customer satisfaction outweigh the risks. Mitigating these risks involve:

To stay ahead of the APP fraud wave, the APAC payments industry can:

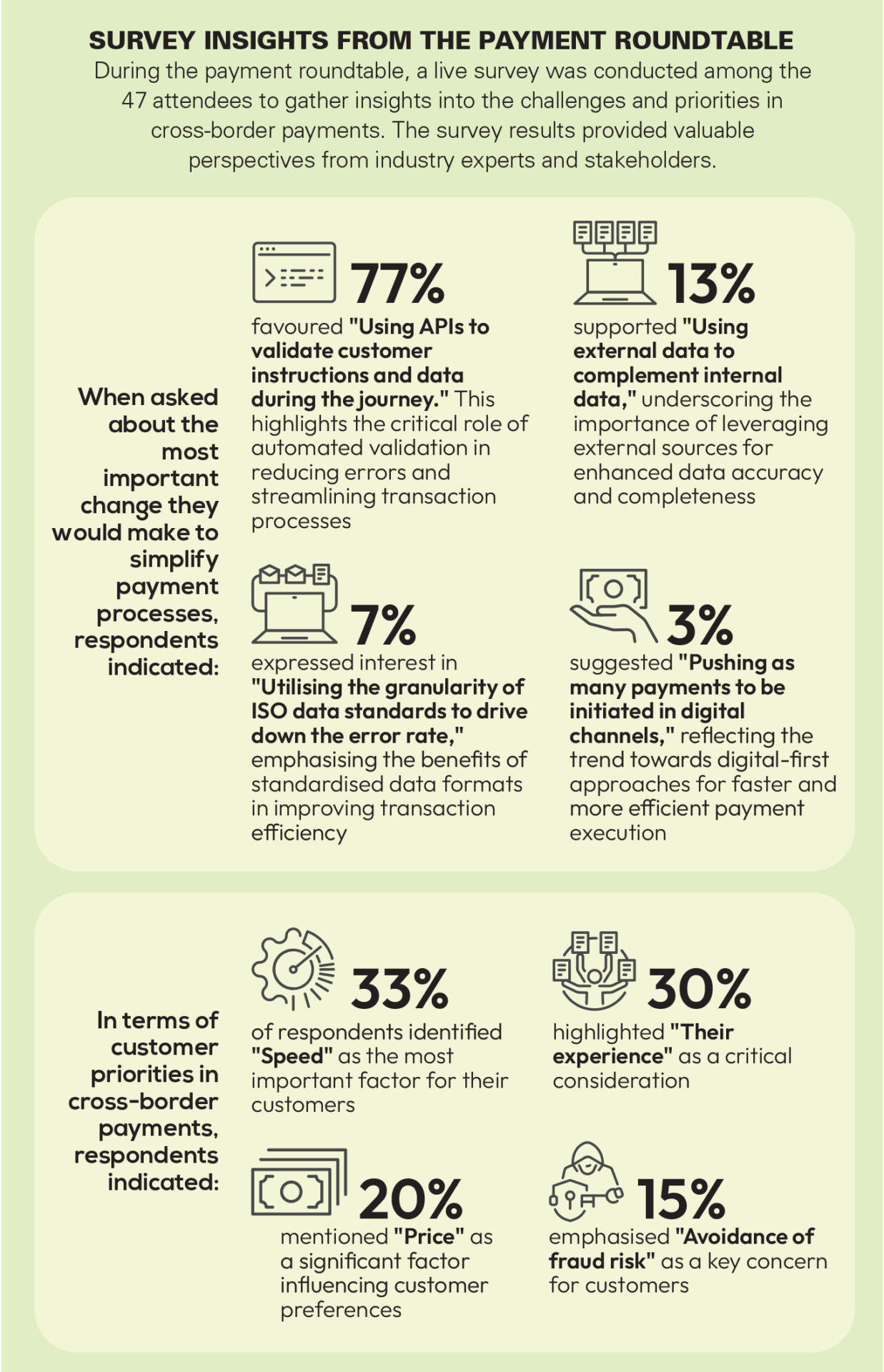

These are the key findings from the roundtable discussion

• Balancing Speed, Safety, and Cost

Achieving frictionless cross-border payments requires balancing the need for speed with safety and cost considerations. Stakeholders must work together to ensure that faster payments do not compromise security or result in higher costs for users.

• Managing Risks and Reducing Friction

Managing risks like fraud while reducing friction for users is a key focus. Advanced security measures, real-time monitoring, and consumer education are essential in this regard.

• Challenges with Domestic Payment Systems

Different domestic payment systems and digital wallets present challenges in achieving seamless cross-border payments. Overcoming these challenges involve developing interoperable solutions and fostering collaboration among stakeholders

• Role of Regulation and Interoperability

Regulation plays a critical role in shaping the cross-border payment landscape. There is a need for harmonised regulations and interoperability between different payment systems to facilitate seamless transactions across borders.

• Collaboration Among Stakeholders

Collaboration between banks, fintech, and regulators is crucial in addressing the challenges of cross-border payments. Joint efforts can lead to the development of innovative solutions and the establishment of standardised protocols.

• Importance of Customer Experience and Transparency

Enhancing customer experience and ensuring transparency on fees and exchange rates are vital for building trust and satisfaction among users. Clear communication and user-friendly interfaces are important components.

• Evolving Role of Digital Wallets and Financial Inclusion

Digital wallets are becoming increasingly important in the cross-border payment landscape. Ensuring financial inclusion by providing access to digital payment solutions for all segments of the population is a key consideration.

• Opportunities and Challenges with New Technologies

New technologies like blockchain and central bank digital currencies present both opportunities and challenges. Leveraging these technologies can enhance the efficiency and security of cross-border payments, but also requires careful consideration of regulatory and technical aspects.

The journey towards frictionless cross-border payments in the APAC region is a complex and multifaceted endeavour that requires collaboration among traditional finance institutions, fintech companies, and governments. Achieving seamless cross-border transactions hinges on striking a balance between speed, safety, and cost. By prioritising interoperability, enhancing customer experience, and implementing advanced security measures, the region can realise the aspiration of making cross-border payments as efficient as domestic transactions. Continued efforts in innovation, regulation, and collaboration are essential to overcoming existing challenges and shaping the future of cross-border payments.

LexisNexis Risk Solutions harnesses the power of data and advanced analytics to provide insights that help businesses and government entities reduce risk and improve decisions to benefit people around the globe. The company provides data and technology solutions for a wide range of industries, including insurance, financial services, healthcare, and government. Headquartered in metro Atlanta, Georgia, it has offices throughout the world and is part of RELX (LSE: REL/NYSE: RELX), a global provider of information-based analytics and decision tools for professional and business customers.