Supporting the Low-Carbon Transition of SMEs: Exploring a Lookback Transition Loan Scheme

Bridging the SME financing gap for green transition.

Bridging the SME financing gap for green transition.

By CHENG Lin, SU Yuqiao, ZENG Yuqi

Small- and medium-sized enterprises (SME) are a critical pillar of a national economy, an essential force in driving a green and low-carbon transformation of the economy and society, and a fundamental basis for many countries to achieve its climate targets. Taking China as an example, public data indicate that the number of SMEs exceeded 140 million in 2020, with approximately 2.52 million new firms established and more than 22,000 new registrations each day, reflecting a highly dynamic and rapidly expanding business landscape. At the macro level, SMEs contribute significantly to China’s economic and social development, accounting for over 50% of tax revenues, more than 60% of gross domestic product, over 70% of technological innovation, around 80% of urban employment, and more than 90% of all registered enterprises. This could be a similar situation for many other economies. Within industrial structures, SMEs operate like ‘capillaries’ reaching the far end of industrial networks, injecting flexibility and robustness into the broader economic system.

SMEs also hold substantial potential in driving the green transition and reducing carbon emissions. While individual SMEs are small compared with large enterprises, their vast numbers translate into significant collective mitigation capacity. Indeed, SMEs are estimated to account for nearly half of carbon emissions in China’s industrial sector, underscoring that their adoption of green practices is critical to achieving national emission reduction targets.

In summary, SMEs underpin economic growth, employment, and innovation while also representing a major lever for emissions reduction. Their active participation in the green transition is therefore essential for achieving broader sustainability objectives. To support this process, targeted financial instruments can help unlock their transition potential, accelerate the greening of the national economy and society.

SMEs rely heavily on external financing, particularly from commercial banks. This dependence makes them especially vulnerable to financing constraints, which continue to hinder their ability to advance green transition efforts. Despite their substantial potential to contribute to the low-carbon economy, SMEs often struggle to secure the sustained and sizable investments required for initiatives, such as equipment upgrades and process improvements. At the same time, existing financing mechanisms impose multiple structural limitations on their access to capital, further constraining their capacity to undertake comprehensive green and low-carbon transformations.

From an accessibility perspective, many SMEs find it difficult to obtain initial loans. The expansion of credit-based lending has been slow, and most firms still depend on collaterals or third-party guarantees — a mismatch with SMEs’ typically small asset base and fluctuating cash flows. Financing costs further compound these challenges. Although the weighted average interest rate on newly issued corporate loans fell to 3.63% in June 2024 and dropped further to around 3.3% for the rest of the year, these reductions have not been fully passed through to SMEs.

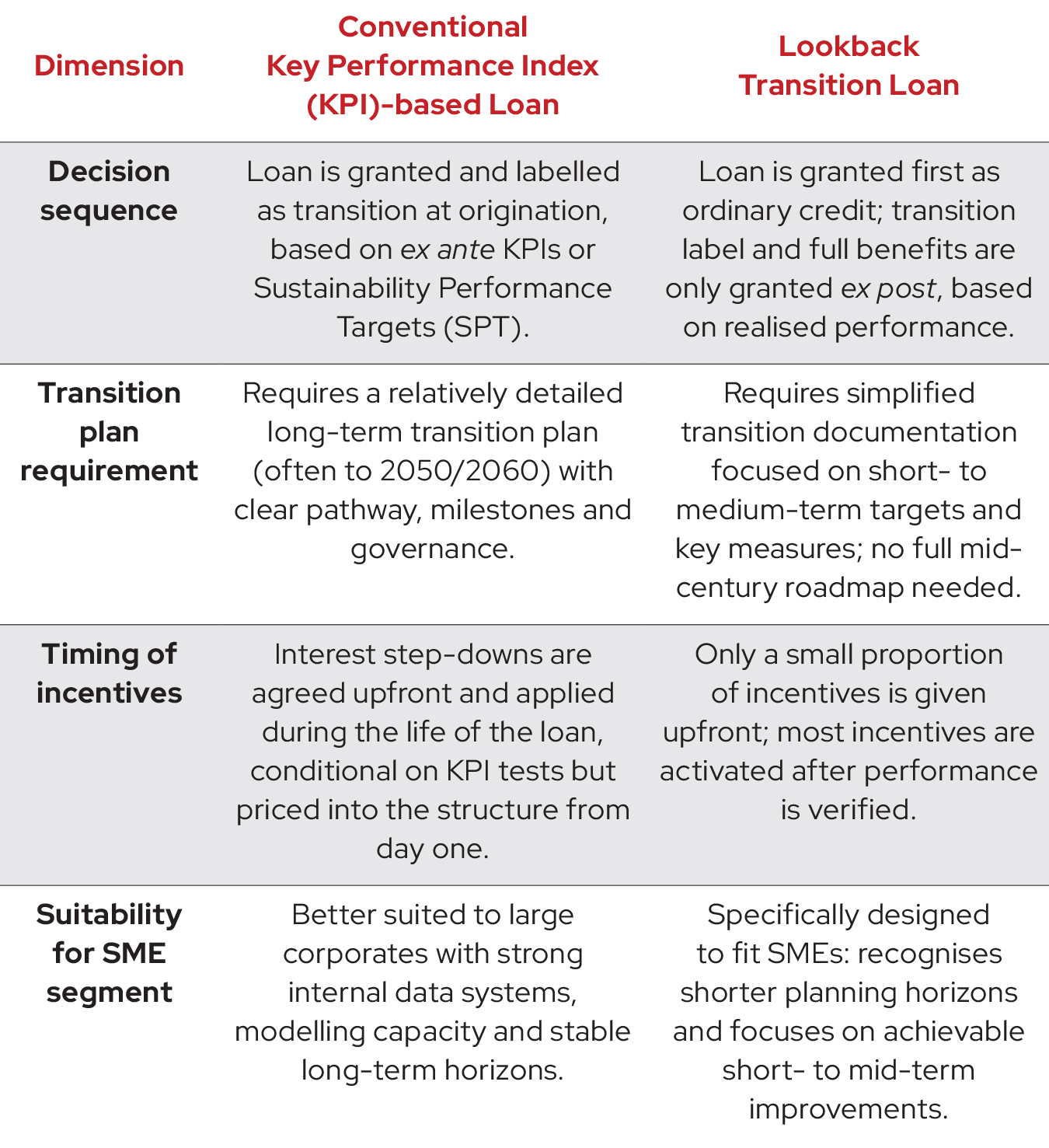

A further barrier lies in the expectations around long-term transition planning. Current market standards and many transition-finance frameworks are geared towards large corporates and require detailed decarbonisation pathways toward 2050 or 2060, underpinned by robust forecast, modelling and governance structures. Most SMEs neither have the technical capacity nor the organisational incentives to produce such plans, particularly given their shorter business planning horizons and higher exposure to market and policy volatility. Requiring SMEs to submit long-term transition roadmaps often result in boilerplate documents that do little to guide real investment decisions and can undermine the perceived credibility of their commitments. Therefore, it is both more realistic and more decision-useful to focus on short- to medium-term targets, supported by financing tools that reward verifiable progress over the nearer timeframes.

On the supply side, the market development of green finance and transition finance has been uneven. By the second quarter of 2025, the outstanding balance of green loans had reached RMB42.39 trillion, a growing by roughly 22% year-on-year and far outpacing overall loan expansion. In contrast, transition finance tools, designed to support upgrades in high-carbon sectors, have progressed only modestly with their total scale remaining below 1% of green loans. These structural limitations create long-term challenges for SMEs in securing financing for green transition and continue to slow their transformation progress.

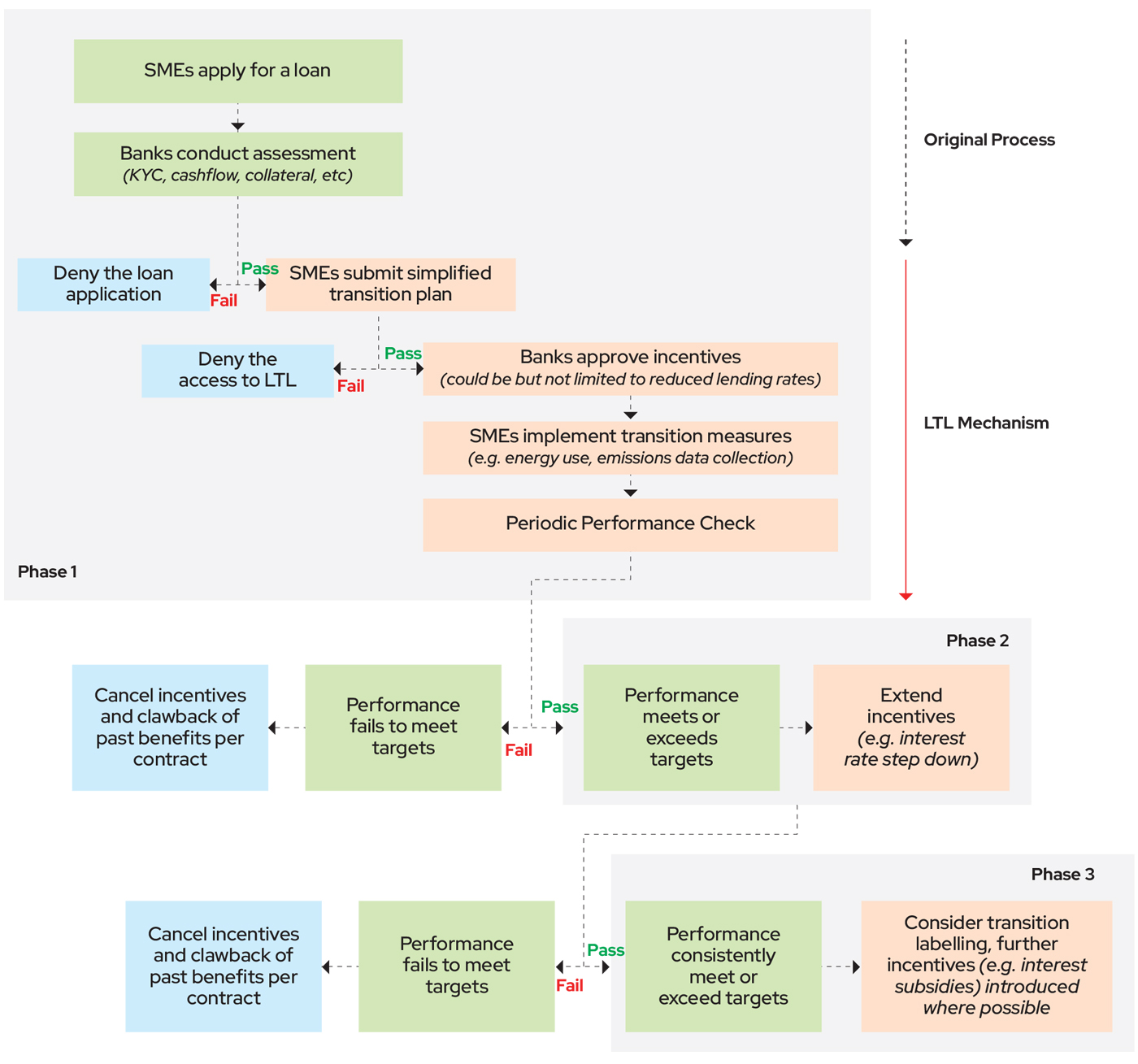

Against this backdrop, the proposed LTL mechanism aims at offering a pragmatic way to reconcile the bank’s risk appetite with SMEs’ need for accessible and affordable finance. The core idea is to lower the front-end barrier and tie the full benefit/incentives to verifiable performance ex post. Instead of requiring a complete long-term transition plan at origination, banks underwrite loans using normal assessing criteria to grant credit. The borrower provides simplified transition documentation focusing on short- and medium-term targets and key measures rather than a fully-fledged pathway on transition (see Table 1).

The distinctive feature of LTL is that incentives are tied to ex post performance. During the life of the loan, the borrower’s progress against measurable indicators, most often emissions-intensity reductions or energy-efficiency gains, is assessed through proportionate verification. When performance meets pre-agreed thresholds, the loan is retrospectively designated as a transition loan and the interest rate is adjusted downwards according to a predefined schedule. If performance is below expectation, the benefit is reduced; in cases of clear underperformance, the concession can be clawed back contractually. In this way, the full advantage of transition finance is ‘earned’ rather than granted upfront, allowing banks to reward real outcomes while limiting exposure to transition washing.

To operationalise this earn-out logic, the mechanism is typically structured into three phases. At the start, the bank decides whether to lend based on its usual credit assessment criteria such as Know Your Customer, cash flow, collateral or other security. At this point, the SME only needs to provide a simplified transition plan with short- and mid-term targets and implementation actions. Once the bank confirms that the SME is creditworthy and the transition plan is credible, it offers a small initial incentive like rate discount to establish the minimum motivation for SMEs actions.

In the second phase, if the borrower achieves the first-year reduction targets, the incentive is maintained or moderately increased. The exact step-up depends on project quality and risk; there is no obligation to offer aggressive concessions. The focus is to secure reliable access to finance and encourage continued engagement, without undermining risk adjusted returns.

In the third phase, for borrowers that consistently meet or exceed their targets, transition labelling would be considered and, where available, interest subsidies or preferential funding lines are layered onto the pricing. Over the full maturity of the loan, cumulative borrowing costs fall below benchmark levels. The differential to the benchmark can be seen as compensation for sustained data disclosure and compliance effort rather than as an unconditional subsidy (see Chart 1).

Effective implementation of LTL requires suitable institutional channels and a supportive policy framework. Under the China context, city commercial banks, rural commercial banks and other local financial institutions are natural first movers. Counties and small cities already concentrate a large share of SME activity, and these banks have deep local client coverage, experience with small-ticket, high-turnover lending and relatively flexible governance. This makes them well placed to pilot LTL into existing SME and green-credit products, especially within designated green-finance and climate-investment pilot zones.

For banks, a successful LTL rollout can help build a pipeline of performance-based transition assets, improve portfolio resilience and support regulatory transition targets without sacrificing risk-adjusted returns. For SMEs, LTL offers a clearer, more realistic path to accessible funding.

The LTL framework must be underpinned by robust risk management and data verification arrangements. Banks should adopt clear internal policies to ensure that concessional pricing is always proportionate to verified transition performance and do not dilute overall returns. Defining unified indicators and sector-specific performance threshold help to keep pricing outcomes transparent and consistent. Another key objective is to minimise transition-washing risk: loans labelled as ‘transition’ should be demonstrably linked to credible decarbonisation.

To support this, banks need processed data tracking and verification infrastructures. Standardised toolkits such as data templates for baselines and emission-factor libraries could be an easy first step. Automated consistency checks comparing energy use with output, or reconciling reported figures with external databases, can be used to flag anomalies and prioritise files for manual review.

Finally, targeted public support and capacity building are needed to complement the financial instrument. Local governments and industry funds can establish shared pools for interest subsidies and fee support, explicitly linked to data quality and verified emission-reduction results. Initiatives such as the Capacity-building Alliance of Sustainable Investment (CASI) offer comprehensive courses and case libraries that can be integrated into banks’ and firms’ training and assessment systems, helping to shorten the learning curve from concept to practice.

Taken together, these measures would allow the LTL to become a practical bridge between SME financing realities and the integrity requirements of transition finance. By lowering front-end barriers, tying material benefits to verified outcomes and embedding the mechanism in a coherent data and policy ecosystem, LTL can align incentives for banks and SMEs and help ensure that transition-finance resources deliver credible, measurable impact.

Capacity-building Alliance of Sustainable Investment (CASI) is a capacity-building initiative that helps financial institutions, regulators, and market participants strengthen practical skills in sustainable and transition finance. CASI convenes global experts and local practitioners to translate standards, tools, and policy developments into actionable learning and implementation support through forums, seminars, technical assistance, and e-learning.