Hedged

As the financial world faces fractures, there is only one safe position.

By Angela SP Yap

When the rules no longer protect you, you must protect yourself.

Months after Canadian Prime Minister Mark Carney’s bold declaration at the World Economic Forum’s (WEF) this year, we are finally seeing how the chips have fallen.

For 17 minutes, the ex-Bank of England governor argued that the “rules-based international order” has fractured, forcing middle powers like Canada – who rank below America and China as superpowers – to strengthen their domestic positions and lean in with new partnerships and allies.

It is good advice for countries, irrespective of whether one is a middle power or emergent one.

Within the last few years, financial markets have roiled as economic instability, political shifts, social polarisation, and overwhelming technological change has shattered long-held beliefs about how our world works. Pundits are no longer talking about financial fragility, but financial fracture – a break from the norms and conventions that have governed us for close to a century.

In Asia’s Role in a World Unhinged, editors Christoph Nedopil and Gloria Ge describe our current situation as “a historic inflection point: a world increasingly ‘unhinged’ from the rules and alliances that governed the last eight decades.”

They predict that formal institutions like the United Nations will continue to exist, but with decreased funding and also with less influence. This leads to an inevitable spillover into finance, where rule and order is replaced with what President Xi Jinping has warned as “the risks of returning to the law of the jungle.”

We already see this unfolding in real time. Over the past year, several major powers and their financial institutions have opted out of global compacts and financial coalitions, bringing decades of sustainability work to a grinding halt. It is a subject we explore in greater detail on page 20 in Battle for ‘Woke Banking’.

But green finance isn’t the only casualty in this era of financial fragmentation. These past two years have seen a rapid rise of financial deregulation in the US and UK, where the separation between supervisory and executive powers are now blurry at best.

This isn’t a shift in the competitive landscape, but an attempt by major powers to throw out the rule book entirely. How can market actors expect to thrive under such unpredictability and short-termism?

Recalibration is the answer. Just as banks in Asia Pacific hedge their trading positions, so must they strategise in ways that ensure the rug isn’t pulled out from under during times of extreme unpredictability.

As Nedopil and Ge express: “For Asia-Pacific decision-makers, adhering to old playbooks now risks sovereign and competitive vulnerabilities. Navigating this era of disequilibrium requires a shift from reactive management to ‘adaptive leadership’ – anchoring action in regional values to secure a peaceful and prosperous future.”

Successful recalibration to this era of fractured finance hinges upon one’s flexibility to adapt on the following critical fronts.

Robert Mundell, the Nobel laureate economist, once asserted that “strong currencies are the children of empires and great powers.” It is a quote of intense meaning because it equates political and military superiority to the global dominance of a nation’s currency. For example, the resurgence of the yen will be directly proportionate to Japan’s military and political might in global terms.

It also means that power is not separate from financial strength.

The current shift towards a multipolar world – where global influence is increasingly distributed between major economies like China, India, and regional blocs such as the Association of Southeast Asian Nations (ASEAN), Asia-Pacific Economic Cooperation, and BRICS+ (Brazil, Russia, India, China, South Africa, and other Asian members) – also means that there are opportunities as well as risk to take into account.

There is already a waning in the use of the US dollar in world trade and financial transactions. Even before the US-Iran war, all reports pointed towards a deliberate diversification away from US dollar holdings, both as a currency of trade and reserve currency. This is supported by statistics from major institutions – the Bank of International Settlements (BIS), International Monetary Fund (IMF), European Central Bank (ECB) – which have all clocked significant reweighting of foreign investments into other currencies such as the euro and renminbi, as well as gold assets.

As early as April 2025, the BIS’ Bulletin No.105 highlighted the US dollar’s slide as foreign exchange hedging amplified depreciation pressures on the currency. Asian investors reduced their currency hedging for US dollar investments due to high costs, which further contributed to volatility. The IMF’s Currency Composition of Official Foreign Exchange Reserves report showed a similar trend with US dollar-denominated global reserves declining to 56.77% as at the fourth quarter of 2025 (Q42025) with long-term diversification towards other currencies.

Other factors such as the higher and arbitrary imposition of tariffs, have also put the US dollar on the backfoot. By now, the most resilient financial institutions would have hedged their positions and strategically reallocated/rebalanced their portfolios away from US assets. These indicators point to the devolving global role of the US dollar.

Consequently, Southeast Asian markets are experiencing upsides to this as investors shift their preferences to different markets and hold assets in more stable currencies.

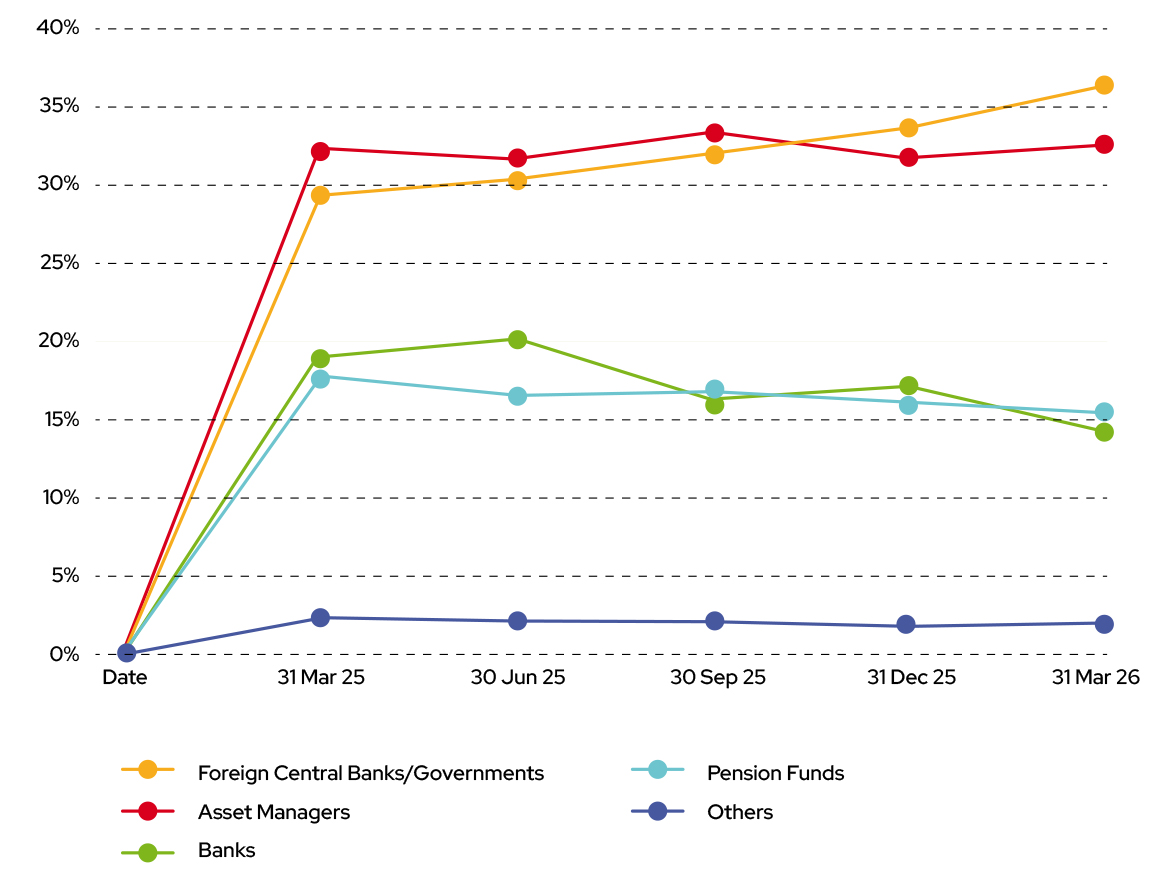

For instance, Figure 1 shows that, as at end March 2026, foreign central banks’ holdings of Malaysian government bonds – comprising Malaysian Government Securities as well as Malaysian Government Investment Issues – stood at 36.1% of total non-resident holdings, representing a 6.4% year-on-year increase.

Think of it as Capitalism 2.0. A reboot of an economic model where climate and social risks are accounted for and investments favour more resilient and equitable options. Where profit generation is indistinguishable from environmental, social, and governance (ESG) goals.

While impact investing and sustainable finance may have been popularised by those on Wall Street and London’s Square Mile over the last two decades, these financial districts have since not just back pedalled, but taken a 180-degree turn.

America’s biggest banks have reeled in their sustainability agenda, breaking away from crucial coalitions. The UK government has shelved plans of a UK Green Taxonomy, pivoting instead towards mandatory transition planning.

The opposite, however, is true in Asia, where almost all jurisdictions are staying the course. These economies are weighing the business case for climate and social justice and have taken the position that sustainability isn’t just ‘good for goodness’ sake’ – the greater benefits to be reaped are multiple and extend far beyond financial firms.

There is an entire green ecosystem that the world has been investing in – climate auditors, fintech challengers, policy advocates, transition industry know-how, taxation experts, and more. These are market actors too who have sprouted and thrived from this burgeoning sustainability movement in finance. What happens to the decades of investments in these industries if the world does an about-turn now?

There is also the reality that Asia-Pacific is the world’s most disaster-prone region. With the higher frequencies of disasters and climate-related displacements taking its economic and human toll, what is urgently needed to close the financing gaps is a nudge in the right direction. When it comes to the ESG proposition, banking policy and priority cannot be ephemeral. It must be a long play. As French agronomist and sustainability leader Minh Cuong Le Quan once said in an interview with this magazine: “There is no banking on a dead planet.”

In a recent interview on Radio Davos, Akshat Rathi, author of Climate Capitalism, described how “it’s now cheaper to save the world than destroy it.” Especially in an interconnected system like financial, a reframing of how we define profit must go beyond ‘traditional’ parameters of efficiency and effectiveness; we must take into account the cost of ethics (or lack thereof) when accounting for the future.

This is more than just semantics. For many idealogues, they tend to pit capitalist values against socialist ones, in a simplistic world view that capitalism works and communism fails. Or for simpletons: America is good, China is bad. But is that the whole story?

Rathi says: “[F]or all the flaws that is China – the world’s largest greenhouse gas emitter, the world’s largest consumer of coal; it is also the world’s largest deployer of all clean energy – solar, wind, the largest maker of electric car batteries, and the largest manufacturer of electric cars.

“The energy transition, for all the blame that India and China get, is also starting to happen in those very places. But those are places which have to take a different tack to try and tackle the climate challenge. They have to figure out the reason for doing this is not just greenhouse gas emissions, but global competitiveness.”

The same can be said of ASEAN. Despite the regional grouping being the world’s most diverse and heterogeneous region, members have somehow found a middle path to bring together the developed economies of Singapore and Malaysia with the less developed economies of Cambodia and Myanmar. It is evidence that solidarity with neighbours can equate to greater stability, market competitiveness, and economic sense.

To illustrate, the release of the fourth and final version of the ASEAN Taxonomy for Sustainable Finance (Taxonomy) last November reinforces its financial-sector commitment to a “resilient, innovative, dynamic, and people-centred” economy by 2045. The market potential for sustainable finance runs into billions of dollars and interoperability between jurisdictions will multiply that figure.

This is because the Taxonomy’s guidelines allow decarbonisation to happen in stages. Transition guidance, such as the ‘grandfathering’ of amber-tier activities (e.g. coal-fired power plants), means that even less-developed-countries such as Cambodia can set out viable pathways and shift from brown to green alongside the mature economies of Malaysia, Singapore, and Indonesia.

As central bank digital currencies (CBDCs) move from pilot to production, economic blocs are already working on unified digital payment ecosystems.

In April 2026, the ECB signed contracts that finalised the technology rules for European card interoperability. This limits the dominance of US-based platforms, Visa and Mastercard, within the Euro system in a bid to minimise exposure to financial disruptions and political pressures.

The EU card network will be free for users, unlike US standards that impose a fee. Plans are also in place for rollout of the digital euro by 2029 in 21 member countries. If parliament approves the digital euro legislation, consultation with EU member states will proceed with a final agreement to be secured by 2027.

Beyond wholesale and retails CBDCs, ASEAN plans for regional QR code interoperability and cross-border transactions executed in local currency. Key initiatives such as Project Nexus, a collaboration led by the BIS and regional central banks, connects domestic instant payment systems via a single hub for near-instant cross-border payments. Go live is targeted in 2027.

Once the nitty gritty of security and interoperability is resolved, digital payment ecosystems like BRICS Pay and countless other bilateral arrangements will foundationally shift the global financial landscape in terms of risk, efficiency, and its eventual players.

This brings into view the need to also secure the technological risks that accompany any CBDC rollout.

There’s a reason why AI is called ‘the $650 billion problem’.

In spite of the staggering investment figure, studies have shown that only 15%–20% of AI projects in finance are deployed; just 8% generate measurable business impact; 35% of failures are the result of poor data quality, and 22% due to integration issues with legacy systems.

These facts don’t seem to fluster markets, as the fixation with AI rallies on.

At the time of writing, Dr Michael Burry, of The Big Short fame who sounded the alarm on the 2008 subprime mortgage crisis, voiced his views on the AI stock market rally via Substack:

“[AI] stocks are not up or down because of jobs or consumer sentiment. They are going straight up because they have been going straight up. On a two-letter thesis that everyone thinks they understand. Feeling like the last months of the 1999-2000 bubble.”

And that $650 billion problem is getting bigger.

To date, Big Tech has invested USD725 billion in AI and the free cash flow of its four biggest companies – Amazon, Alphabet, Microsoft, Meta – is at its lowest point since 2014. These hyper scalers (large cloud service providers) are all-in on AI, backed by syndicated deals to finance expansion of data centres and algorithm refinement. At the time of writing, JP Morgan just announced its exit from a USD4 billion AI centre debt, following similar announcements by other financial firms, especially those backed by private credit. The Financial Stability Board, in concert with several other standard-setters, have warned about the concentration risk and unprecedented credit backing for AI data centres. What is holding, however, are the valuations of AI-related for ‘shovel stocks’ i.e. AI component-makers, like Nvidia, indicating that investments in AI are forking with major banks offloading capex-intensive infrastructure buildouts.

On the talent front, financial firms are also hedging their risks when it comes to hiring. Gillian Tett recounts her recent interaction with a New York financier in FT Weekend on why, for the first time, the company is changing its hiring patterns and making offers to graduates from the humanities instead of science, technology, engineering, and mathematics students.

While these AI-native graduates seemed wildly impressive on paper, the executive told Tett that, “When senior financiers later proved their ideas they found them alarmingly shallow.”

“We want critical thinking, not just AI.”

“[A]s AI fever sweeps finance, it is neither delivering the profit nirvana predicted by tech evangelists nor hastening the doom the Cassandras have warned about…”

Owning up to the harsh reality of the AI hype means coming to terms that the reality is miles apart from the hype. For professionals who have actually introduced and used the tools in their work environments, the results have been dismal.

The real and immediate risk is, as pointed out by the FSA, the likelihood of massive defaults when the AI bubble bursts.

Understanding the changes on these, and other, fronts will help banks in Asia spread their risk, banking on a ‘middle position’ that involves diversified partnerships, deepened intraregional collaborations, and maintaining strategic ambiguity.

Hedging one’s bets is the way to embrace this new, fractured financial order.

Angela SP Yap is a multi-award-winning strategist and social entrepreneur championing Asian perspectives in global conversations. Through her editorial consulting firm, Akasaa, she transforms regional insights into compelling narratives that bridge business, policy, and culture – shaping industry discourse with a distinctly Asian lens grounded in economic analysis and cross-sector expertise.